- If the recent US–Iran deal evolves into a durable resolution, the energy shock is expected to have a limited overall impact on economic growth, though inflation will stay elevated for a while.

- AI investment has been a factor supporting growth across advanced economies, offsetting much of the negative impact from higher energy prices by supporting business spending, manufacturing activity, and financial markets — especially in the US and Japan.

- Across most scenarios, AI-driven investment resilience prevents a major slowdown or recession, keeping global growth broadly stable.

- Only in the permanent disruption scenario does this resilience break down, as sustained energy constraints overwhelm AI investment and lead to recessions in most advanced economies.

Despite a recent diplomatic breakthrough, geopolitical tensions in the Middle East remain a key source of uncertainty for the global economy. The energy supply shock caused by the effective close of the Strait of Hormuz, a critical shipping route for global oil and gas supplies, has highlighted the vulnerability of energy markets and global supply chains to regional instability. Although the recent deal between the US and Iran to reopen the Strait of Hormuz and extend the ceasefire by 60 days has increased the likelihood of a gradual normalisation of energy markets, the prospect of renewed disruptions remains elevated. Reaching a comprehensive agreement on Iran’s nuclear programme within 60 days will be challenging, and any setback in negotiations could quickly reignite tensions.

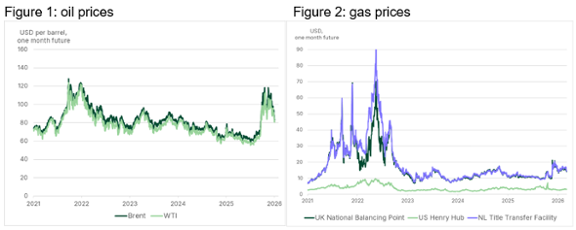

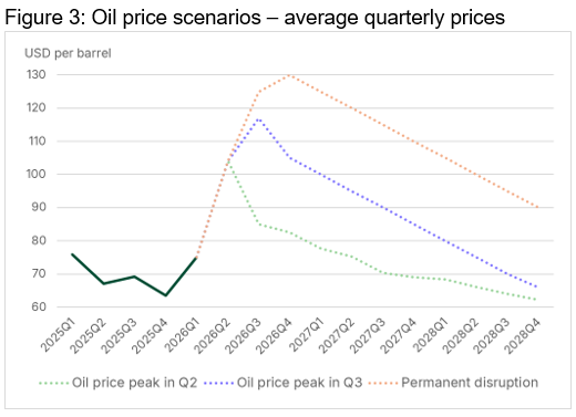

Since the start of the conflict, global oil and gas prices have remained elevated, although the recent agreement has accelerated the downward trend observed in recent weeks (Figures 1 and 2). Governments have responded by drawing on strategic petroleum reserves and encouraging fuel switching towards coal and renewable energy sources. Increased production and exports from oil producers outside the Middle East, particularly the US and Russia, has also helped to limit price rises. Nevertheless, a prolonged delay in the full reopening of the Strait of Hormuz could lead to a significant drawdown in global oil inventories, placing increasing pressure on major economies later this year. Shipowners have already indicated that normal shipping operations will not resume until they are confident that the agreement between the US and Iran is durable and enforceable.

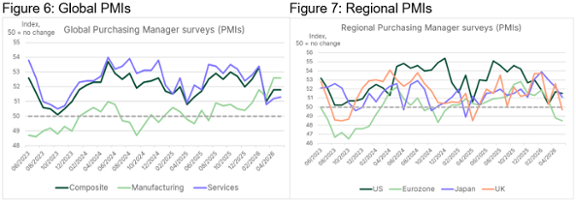

Against this backdrop, we consider three scenarios for how the conflict may evolve and the implications for the global economy. Economically, the main direct channels through which these scenarios impact the economy are energy and agricultural commodity price paths and the size of the confidence shock to the global economy. Together, these factors determine the outlook for inflation, economic growth and policy responses.

The three scenarios are (see Figure 3):

- Oil price peak in Q2: The current deal holds and evolves into a more durable agreement, allowing a gradual reopening of the Strait of Hormuz. Oil, gas and agricultural commodity prices peak in Q2 and return to pre-conflict levels in the second half of 2027. Business confidence weakens modestly, reflected in a temporary increase in the investment risk premium of 0.5 percentage points.

- Oil price peak in Q3: Negotiating a more durable resolution proved more difficult, renewing tensions and resulting in intermittent military strikes that cause further damage to energy infrastructure. A more durable resolution is not reached until late Q3 at the earliest. Oil, gas and agricultural commodity prices peak in Q3 and do not return to pre-conflict levels until 2028. The investment risk premium rises by 1 percentage point until the end of 2027.

- Permanent disruption: The conflict flares up again and escalates into a broader regional war, including attacks on energy infrastructure and potential US ground involvement. Although major hostilities end late 2026, Iranian control of the Strait persists and normal shipping flows recover only partially during 2027. Oil, gas and agricultural commodity prices peak in Q4 2026 and do not return to pre-conflict levels during our forecast horizon. The investment risk premium rises permanently by 2 percentage points from Q4 2026 onwards.

In the remainder of this outlook, we assess the implications of these scenarios for inflation and economic growth across the major advanced economies.

Inflation rises across advanced economies

Higher energy prices have already begun to feed through to consumer prices across advanced economies. The impact has been most visible in the US and the eurozone, where both headline and core inflation have increased since the start of the conflict. Inflation has been somewhat more contained in the UK and Japan, partly because government subsidies have softened the direct impact of higher energy costs.

Looking ahead, the inflationary effects of the energy shock are broadly similar across advanced economies in the different scenarios (Figures 4 and 5). Different outcomes mainly reflect varying starting points and government subsidies rather than major differences in transmission mechanisms.

Under the oil price peak in Q2 scenario, inflation reaches its highest level in 2026 before gradually moderating as energy prices normalise. While inflation remains somewhat above central bank targets, policymakers largely look through the temporary rise in prices, judging that underlying inflation pressures remain contained. Concretely, we expect the BOE and Fed to refrain from hiking rates. The European Central Bank (ECB) is a partial exception, as its relatively accommodative starting position allows for modest insurance rate hikes, bringing the policy rate to 2.5 percent.

In the oil price peak in Q3 scenario, inflation proves both higher and more persistent. The prolonged period of elevated energy and commodity prices keeps headline inflation above target throughout much of 2027, raising concerns that higher costs could become embedded in wages and inflation expectations. As a result, central banks feel forced to tighten policy. We expect the Federal Reserve and the Bank of England to raise policy rates to around 4.25 percent, while the ECB increases its policy rate to 3 percent.

The permanent disruption scenario presents the most challenging environment for the global economy. Persistently elevated energy prices generate considerable second-round effects, causing inflation to remain well above target for an extended period. Central banks are therefore forced to tighten policy more aggressively despite weakening economic activity, with policy rates being hiked by more than one percentage point.

Global growth supported by AI-investment

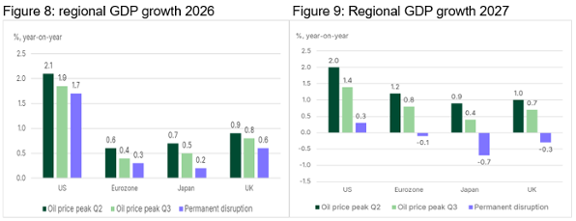

Despite the energy supply shock, economic activity has so far proved remarkably resilient. Business surveys continue to point to an expanding global economy, supported in particular by strength in the manufacturing sector (Figure 6). Part of this resilience reflects firms bringing forward purchases to protect themselves against potential shortages and further increases in energy costs later on. More importantly, however, is that the global economy continues to benefit from a surge in business investment related to artificial intelligence (AI).

Evidence of this trend is visible in countries that play a central role in the AI value chain, most notably the US and Japan. Business surveys for the manufacturing sector in these economies have strengthened considerably, reflecting robust demand for semiconductors, data-centre infrastructure and related technologies. Capital expenditure plans among the world's largest technology companies also continue to be revised upwards, which underpins investor enthusiasm. This enthusiasm has already resulted in global equities largely recovering from the declines that followed the outbreak of the conflict, with US equity markets even reaching new highs. The rising US household wealth resulting from strong equity market performance has in turn likely provided continued support to consumer spending.

Beneath the relatively strong global picture, however, important regional differences remain. In Europe, temporary strength in manufacturing has been more than offset by weakness in the services sector (Figure 7). The eurozone has indeed as the only major advanced economy consistently recorded downside surprises in economic data since the start of the conflict. But if the conflict escalates again, we also expect weakness to materialise elsewhere.

AI investment resilience: powerful but not unlimited

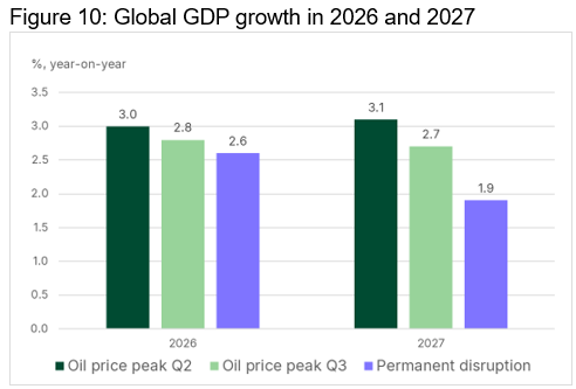

While inflation outcomes are broadly similar for the major advanced economies across the scenarios, the growth impact differs more significantly (Figures 8 and 9). The difference can be explained by the terms of trade. Net energy importers such as the eurozone, the UK and Japan face a deterioration as higher import costs reduce national income. These losses are mirrored by gains for net exporters like the US. However, depending on the scenario, these exporter gains are partly or fully offset by higher domestic inflation, physical supply shortages and a negative global confidence shock, which dampens consumption and investment. Also, the extent to which AI investment can continue to offset the energy shock in heavily AI-exposed countries depends critically on the duration of the energy disruption.

In the oil price peak in Q2 scenario, the growth impact remains limited. A gradual reopening of the Strait of Hormuz allows energy prices to normalise, while strong AI-related investment continues to support business spending, financial markets and global demand. Although growth slows somewhat more in energy-importing regions such as the Europe and Japan, global growth remains broadly in line with the pace seen in recent years.

In the oil price peak in Q3 scenario, resilience begins to weaken, particularly in energy-importing economies. Global growth slows to a pace that is below the trend of recent years. Prolonged energy-market disruption, higher financing costs and elevated uncertainty increasingly weigh on investment and confidence. Nevertheless, continued AI spending and policy support help advanced economies to avoid recession by a comfortable margin.

The limits of AI-driven investment resilience are reached in the permanent disruption scenario. AI investment can offset a relatively short-term global energy shock, but AI investment itself ultimately also depends on stable energy and raw material supplies, favourable financing conditions and business confidence. Persistent energy disruptions undermine all three, especially because AI infrastructure is highly energy-intensive, increasing its vulnerability to sustained energy shortages and elevated electricity prices.

Consequently, AI is no longer able to compensate for the broader drag from higher energy costs, weaker confidence and tighter financial conditions. All major advanced economies except for the US fall into recession, while global growth slows sharply despite additional fiscal support. Prolonged sizable fiscal support is hampered by government bond yields rising strongly, putting especially the UK government in a bind.

Energy security key to long-term wellbeing

Strong investment in AI and related infrastructure, together with investor optimism about future productivity gains, has helped support economic activity and financial markets, cushioning the impact of the energy shock. Yet it remains uncertain whether AI will ultimately deliver the productivity gains currently embedded in market expectations. If not, the market bubble will burst, causing both a confidence shock and an abrupt halt to AI investment. But even if it does deliver, the technology is unlikely to reduce exposure to energy shocks. On the contrary, the rapid expansion of data centres and other AI-related infrastructure is expected to drive a substantial increase in electricity demand over the coming years, making access to reliable energy an increasingly important economic constraint.

For Europe, much attention is focused on its position in the global AI race. However, the current crisis suggests that its central challenge is not so much how to rapidly expand AI capacity, but how to strengthen energy resilience. Long-term wellbeing depends on the availability of secure, affordable and sustainable energy. This reinforces the case for accelerating the energy transition through greater investment in renewable energy, energy efficiency and electricity networks. Reducing energy demand, for example by phasing out low value added and energy intensive forms of production, could speed up the road to energy security. By reducing dependence on imported fossil fuels, Europe can strengthen its resilience to future geopolitical shocks while supporting a more sustainable and secure foundation for long-term prosperity.