- The energy shock following the war in the Middle East has hurt emerging markets’ economic activity and materially increased inflation. Several factors have softened the blow. The AI revolution has helped to keep global demand resilient and governments have stepped in with subsidies, energy-saving measures and renewables to cushion the impact.

- Our reference scenario is based on a sustained peace agreement between the US and Iran. Although the humanitarian toll, infrastructure damage and production losses are irreversible, the wider economic fallout has so far stopped short of recession. We expect emerging markets’ GDP growth to slow and inflation to continue rising throughout the year.

- Given the uncertainty, we set out two downside scenarios. Peace remains fragile amid deep mistrust in the Middle East, unresolved trade tensions with the US and persistent food price pressures linked to the cautious reopening of the Strait of Hormuz. Together, these factors mean that a more prolonged conflict cannot be ruled out.

- The silver lining is that the energy shock is accelerating the shift to renewables, with solar, storage and electric vehicle adoption rising rapidly across Asia, Africa and Latin America. China’s dominance in clean energy production is helping sustain demand.

Several factors helped absorb the shock

When the energy shock hit the world, emerging markets were in relatively strong economic shape. The prolonged closure of the Strait of Hormuz is undoubtedly adding to inflationary pressures, but the impact on global GDP growth has been relatively contained, except in Middle Eastern countries, where the damage has been significant.

The shock has been cushioned by Middle Eastern oil producers using alternative export routes, while other producers, especially the US, have tapped strategic reserves and increased exports to offset global supply losses. Lower oil imports across many countries, including China also helped reduce oil price pressures. Repeated assurances from the US administration that a resolution was near also helped contain price rises.

Emerging market governments have introduced support measures to shield households and businesses from rising direct and indirect costs. In Asia, the hardest-hit region, policy responses broadened quickly, ranging from energy-saving measures such as remote working and four-day weeks to faster renewable energy deployment. As in previous shocks, countries with greater fiscal space and stronger buffers were better placed to respond.

At the same time, the global AI boom, led by the US and reinforced by China’s rapid adoption, has supported US investment and equity market returns, helping to keep global growth resilient. Emerging markets connected to AI-driven economies have benefited through strong trade flows and commodity price gains. China’s high-tech exports, for example, have risen for seven consecutive months.

The key question is how long these combined factors can cushion the near-term impact of the Middle East conflict on emerging markets and what they imply for long-term risks.

Revising our scenarios

We are updating the scenarios we published in April 2026. At that time, our most optimistic scenario assumed that an agreement would be reached sooner. Since 28 February, Brent prices have averaged USD 100 per barrel, having peaked in April for now and moved close to USD 80 since the recent announcement of a peace agreement in June. Our adjusted global scenarios are built around different expectations for oil price paths:

- Reference scenario: Oil prices peak in Q2 and return to pre-conflict levels in the second half of 2027. This scenario is based on the prospect that the agreement recently reached to end the war on Iran will be sustained. So far, the agreement envisages a two-step approach, with a 60-day phase to determine the future of Iran’s nuclear programme (see Outlook section below for emerging markets impact).

- Oil prices peak in Q3: This intermediate scenario assumes that oil prices peak in Q3 and only ease towards pre-conflict levels in 2028. We think the sensitivity of the discussion around Iran’s uranium enrichment under this scenario could drag on into late Q3, with tensions lasting until then. Under this scenario, GDP growth of the two largest emerging economies - China and India - would decline moderately in 2026 and 2027. Both countries would probably rely more on alternative energy sources, including coal and new fuel blends, to support growth.

- Permanent disruption: If military action resumes and continues through the year, oil prices could peak in Q4. Further damage to oil infrastructure would likely push any return to pre-conflict price levels beyond our forecast horizon. Both China and India would face a sharp slowdown in GDP growth in 2027, reflecting the prolonged conflict. China would be hit harder than India, given its greater exposure to the global slowdown as a result of its strong trade linkages.

The outlook

Based on the reference scenario, including mitigating actions to reduce the conflict’s impact and the AI investment cycle continuing through the rest of 2026, which should increase global demand for commodities and inputs from a wide range of countries, we expect emerging market economic activity growth to slow modestly to 3.7% in 2026, from 4.4% in 2025. Growth divergence across countries is expected to persist. The Middle East, in particular, is close to contraction. Meanwhile, inflation is likely to become more material in the second half of the year. High inflation is being driven by firming food price pressures and transport costs, while services inflation signals are mixed due to weakening demand. We expect the average inflation rate to reach 5.4% in 2026, which is 1.2 percentage points above pre-conflict forecast levels.

Given the breadth and diversity of emerging market economies, we focus on the key impacts of our reference scenario for the remainder of this outlook.

Diverse impact across emerging countries. Economic activity in the Gulf Cooperation Council (GCC) countries is expected to contract by more than 1% in 2026. Qatar and Kuwait, for example, are facing oil production cuts and infrastructure damage. Other countries are better positioned because they have alternative export routes. Oil-exporting countries with domestic refining capacity outside the Middle East, such as Nigeria, Ghana, Azerbaijan, Kazakhstan and Colombia, will benefit from higher fossil fuel prices. However, some oil exporters import oil derivatives, and their net windfall gains will be modest, as derivative prices are rising much faster than oil prices. Angola and Ecuador are already facing fuel shortages because of limited domestic refining capacity, forcing them to import expensive refined products such as petrol.

Some oil importers will be able to partly offset higher fossil fuel import costs through stronger export revenue from commodities linked to the AI investment surge. Chile and Peru, for example, are benefiting from high copper prices. Another group of oil importers, including Georgia, Armenia and India, has kept energy prices fixed through government subsidies for some time, limiting the impact on consumers for now. However, economic activity in these countries is likely to slow in the second half of the year as limited fiscal capacity forces governments to scale back these subsidies.

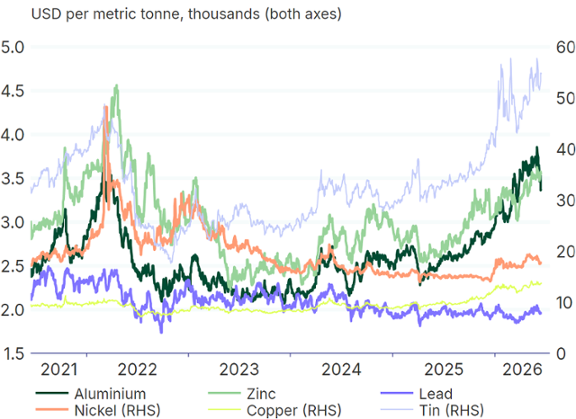

Base metals prices

At the other end of the spectrum, net oil and fuel importers with no fossil fuel reserves and limited fiscal room for support at the start of the conflict are under acute pressure from high fuel prices. Emerging Asian countries generally fall into this category and have been hit particularly hard, including the Philippines, Sri Lanka and Cambodia.

China’s growth prospects. China’s growth rate has surprised on the upside over the past few quarters. The broadening AI revolution is sustaining China’s export momentum and China-linked supply chains. In addition, the energy shock is increasing demand for clean energy and, with it, the world’s dependence on China as a key producer of clean energy technologies. This may exacerbate tensions with China’s trade partners. This is already evident in the new US Section 301 tariffs, which aim to address forced labour concerns in 60 countries, including China.

On top of this, the EU’s stance on China is becoming tougher from a security perspective. Meanwhile, we think the energy shock will remain manageable for China, given that it is less dependent on Gulf countries than many other Asian countries. China will likely continue to increase coal demand to offset the loss of oil imports for as long as needed. As a result, we think China’s growth will slow modestly to 4.5% year on year in 2026, mainly driven by weak domestic demand.

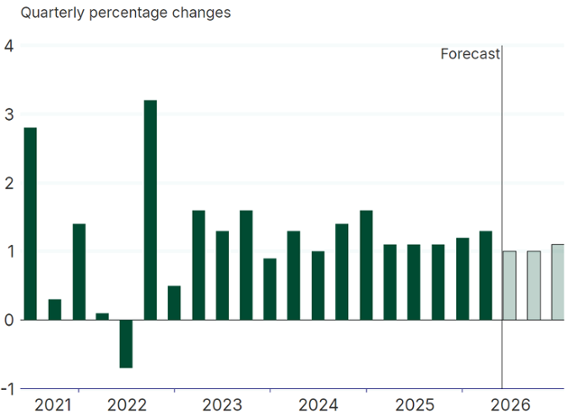

China GDP

Rising inflation. The inflationary impact of the oil shock on emerging markets remains material in oil-importing countries with limited fossil fuel reserves. As a rule of thumb, a sustained USD 10 increase in oil prices ultimately adds 0.3–0.4 percentage points to emerging markets’ headline inflation. Emerging markets are more exposed than developed markets because food carries a larger weight in their inflation baskets.

Food prices are already rising due to higher shipping costs and elevated domestic fuel and fertiliser prices, affecting mostly countries with a high dependence on fertiliser imports, such as India and Romania. In India, domestic fertiliser plants are struggling to secure inputs, while a surge in demand and expectations of shortages are adding further price pressure. There is a risk that fertiliser shortages will have a lasting effect on food prices, as any crop production loss or lower yields cannot be recovered. In addition, the odds of a strong El Niño towards the end of the year are rising, which could further disrupt food production and put pressure on inflation expectations.

Central banks’ role. To counter rising inflation, central banks will feel compelled to raise rates. Yet higher interest rates will further drag on growth, adding to the negative effects of the initial supply shock. This means emerging market central banks are walking a tightrope. Several are under financial market pressure to tighten policy, especially as the prospect of higher interest rates in major advanced economies weighs on their currencies. The Philippines, Indonesia, South Africa and Pakistan have already raised rates and are expected to tighten further. Therefore, the jury is still out on whether central banks will be able to halt second-round effects and tame inflation expectations.

Fiscal and international support. Government support is the first line of defence to protect the most vulnerable, but it is gradually being scaled back with the duration of the conflict. Most measures were temporary, reflecting the expectation that the shock would be transitory. Latin American governments have largely shielded consumers and strategic sectors from the oil shock with fuel subsidies. In Colombia, however, fiscal risks remain elevated as the underlying position continues to weaken. In contrast, Chile has prioritised fiscal consolidation, limiting its policy response. Indonesia faces a fiscal target and is under financial stress as pressure mounts to lift the fiscal deficit target. India is also reducing fuel subsidies because of the increasing fiscal burden and putting tariff on gold to protect the rupee. Other countries are likely to encounter similar fiscal limits and it will be in many cases remittances that will be used to stabilise incomes.

At the same time, international financial institutions are preparing to provide funding to an increasing number of countries. In June, at least 15 Asian countries applied for funding from the Asia Development Bank, including the Philippines and Sri Lanka. Some of the funding is intended to finance clean energy access. The IMF expects at least a dozen countries to seek loan programmes in the coming months, while the World Bank is making capital available to support social safety nets for the most vulnerable people, boost fiscal capacity and provide working capital and liquidity support for firms and farms. This type of funding becomes critical when domestic resources begin to dry up.

Renewed momentum for the energy transition. The need to reduce dependence on the Middle East is encouraging greater investment in domestic renewable energy capacity and other energy sources, including nuclear and coal. Countries such as the Philippines, South Africa, Thailand and Nigeria facing varying levels of energy supply disruption, are accelerating the adoption of solar power and energy storage solutions. China’s leading role in renewables and its large investments have allowed it to respond quickly to this demand, making renewables an increasingly important source of its export strength.

This overall increase in demand for renewables is likely to persist because governments have started embedding renewable energy use in regulations. These initiatives aim to give investors more stability. India, the Philippines and Mexico are fast-tracking renewable energy projects and providing incentives to increase demand for renewables. El Niño adds another incentive, as drought-related hydropower risks increase and, with them, the need for more reliable energy sources. Ecuador is reviewing this alternative based on the past impact of El Niño.

Nevertheless, challenges remain. Many emerging Asian countries have increased coal usage to offset oil and gas supply disruptions. Coal is an important domestically available fossil fuel source in the region. In the coming time, government price signals will be important in guiding energy choices. Higher borrowing costs, inflationary pressures and infrastructure bottlenecks in connecting renewable energy projects to grids are other challenges that emerging markets face.

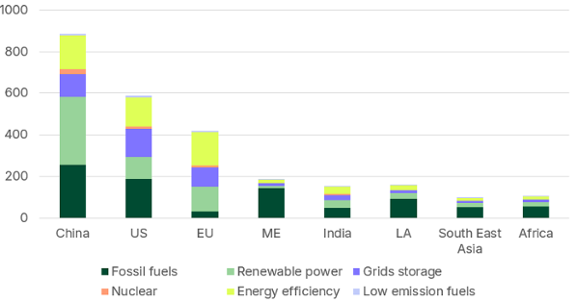

Energy investments in USD billion

Conclusion

Emerging markets have beaten expectations in recent years, navigating global turbulence without major debt or currency crises. This resilience has been driven by stronger fundamentals, central bank credibility, flexible exchange rates and in many cases disciplined debt management. However, the impact of the Middle East conflict will not quickly fade. More thought must be given to how to avoid a new crisis. The lessons from this conflict are clear: energy is no longer just a commodity; energy security is now a cornerstone of society. Consequently, building renewable energy capacity is crucial.

But the opportunity for cooperation and fairness extends beyond energy. The next frontier is fair AI, allowing emerging markets to leapfrog outdated models of consumption-driven growth. For investors willing to be part of this change, this means investing in technology that combines fairness with innovation. Both renewable energy and AI matter for emerging markets and for the world as it seeks to avoid the next crisis.

Forecasts selected countries

| GDP growth (% yoy) Inflation (CPI, % yoy avg) | |||||||

|---|---|---|---|---|---|---|---|

| Prelim. | Forecast | Prelim. | Forecast | ||||

| 2024 | 2025 | 2026 | 2024 | 2025 | 2026 | ||

| Bolivia | -1,1 | -1,2 | -2,2 | 5,1 | 19,5 | 17,1 | |

| Brazil | 3 | 2,6 | 1,6 | 4,4 | 5 | 4,7 | |

| Chile | 2,6 | 2,6 | 2 | 3,9 | 4,2 | 4,1 | |

| China (mainland) | 5 | 4,9 | 4,5 | 0,2 | 0 | 1 | |

| Colombia | 1,5 | 2,6 | 2,1 | 6,6 | 5,1 | 6,6 | |

| Ecuador | -1,9 | 3,7 | 2,5 | 1,5 | 0,7 | 3,1 | |

| India | 7 | 7,4 | 6,3 | 4,9 | 2,2 | 5,4 | |

| Indonesia | 5 | 5,1 | 5,2 | 2,3 | 1,9 | 3,1 | |

| Ghana | 5,7 | 6 | 5 | 22,9 | 14,2 | 5,2 | |

| Kazakhstan | 5 | 6,5 | 4,6 | 9 | 11,4 | 12 | |

| Kenya | 4,7 | 4,9 | 4,6 | 4,5 | 4,1 | 6,4 | |

| Mexico | 1,1 | 0,8 | 0,6 | 4,7 | 3,8 | 5,2 | |

| Pakistan | 3 | 3 | 3,3 | 12,6 | 3,5 | 8,3 | |

| Peru | 3,5 | 3,4 | 2,7 | 2,4 | 1,5 | 3,6 | |

| Philippines | 5,6 | 4,5 | 4,1 | 3,2 | 1,6 | 6,8 | |

| Poland | 3,1 | 3,7 | 3,4 | 3,7 | 3,6 | 3,4 | |

| Russia | 4,3 | 1 | 1,2 | 8,4 | 8,7 | 6,2 | |

| South Africa | 0,5 | 1,1 | 0,9 | 4,4 | 3,2 | 4,6 | |

| South Korea | 2 | 1 | 1,7 | 2,3 | 2,1 | 3,1 | |

| Thailand | 2,9 | 2,4 | 1,4 | 0,4 | -0,1 | 2 | |

| Turkey | 3,5 | 3,6 | 2,6 | 58,5 | 34,9 | 32,4 | |

| Uzbekistan | 6,5 | 7,7 | 8,1 | 9,6 | 8,8 | 7,6 | |

Source: S&P Global/Triodos Bank