- Global supply shock lifts inflation broadly across countries: Disruption in the Strait of Hormuz drives higher energy and food prices worldwide, with similar inflation impacts across both energy importers and exporters, as global price transmission dominates national differences.

- Growth diverges much more than inflation: While the inflationary impact is broadly uniform, economic growth effects vary more strongly. Energy importers (Japan and Europe) suffer the largest losses, while exporters like the US are relatively more shielded unless the shock becomes severe.

- Outcomes depend on duration and escalation: A gradual reopening of the Strait of Hormuz limits damage to a temporary global growth slowdown, prolonged disruption requires policy support and weakens growth further, while a permanent disruption risks persistent inflation, severe financial market stress, and global recession.

- Europe should respond strategically, not reactively: Rather than broad subsidies or aggressive rate hikes, policymakers should focus on targeted support and accelerating the energy transition to reduce structural dependence on imported fossil fuels.

The war of the US and Israel against Iran has presented the global economy with yet another sizeable shock. The immediate driver of this shock is the effective closure of the Strait of Hormuz by the Iranian military. About 20 to 30 percent of world’s oil and liquefied natural gas (LNG) usually passes through this 50 kilometre wide sea strait. Asia is the primary destination, receiving nearly 90 percent of both oil and LNG. Crude oil from the Middle East makes up about 60 percent of Asia’s total oil imports. China, India and Japan are being the main importers of oil, but as a percent of total national oil consumption South Korea, Japan and India are most exposed.

Europe is the second-largest destination, receiving the remaining 10 percent of LNG transported through the Strait. In 2025, LNG flows via Hormuz accounted for around 27 percent of Asia’s imports and about 7 percent of Europe’s.

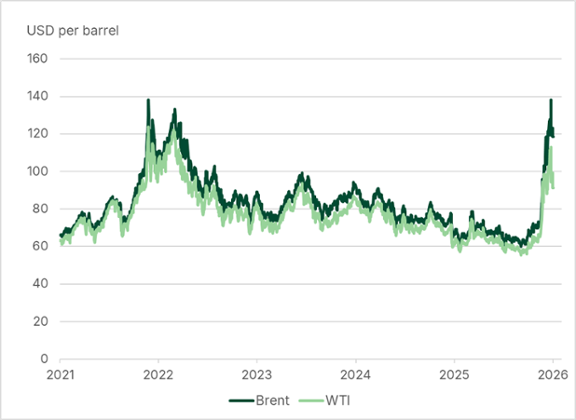

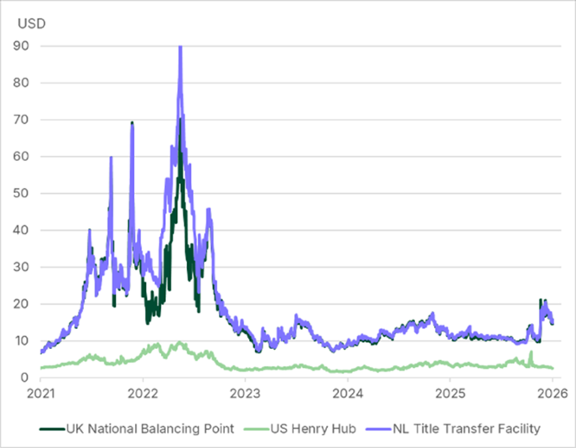

As a result of the war, global oil and gas prices have risen sharply (Figures 1 and 2). Oil prices briefly approached levels seen during the 2022 energy crisis, while European gas prices remain well below those peaks. At first sight, net energy exporters not directly affected by the conflict, such as the US, Canada, Brazil, Australia, Indonesia and Russia, seem relatively insulated and may even benefit compared to net importers.

However, the situation is more complex than energy alone. Roughly one-third of global fertiliser shipments also pass through the Strait, threatening agricultural yields just as the Northern Hemisphere planting season begins and pushing food prices higher. The Middle East is also a key supplier of helium, essential for semiconductors and medical imaging, meaning disruptions extend beyond energy markets.

The severity of the inflation shock depends on the duration of the conflict and the extent of infrastructure damage. Even undamaged LNG facilities are particularly difficult to restart, implying that supply will remain constrained for several weeks even after the Strait reopens. Oil production may recover more quickly but will still face delays. The International Energy Agency reports that around 40 energy assets across nine Middle Eastern countries have already been classified as severely damaged, raising the risk of prolonged global energy supply disruptions even if the ceasefire holds.

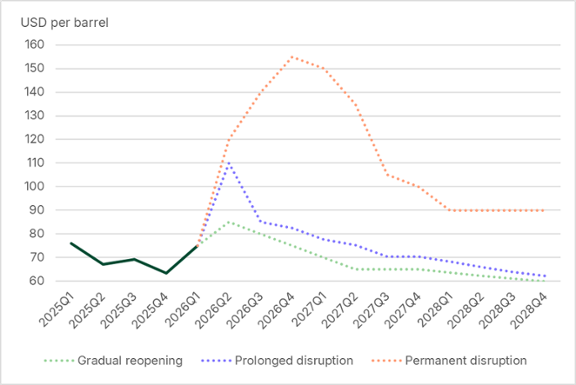

A temporary two-week ceasefire between Iran and the US has so far not resulted in the reopening of the Strait of Hormuz, and negotiations so far have been fruitless. Therefore, a lasting resolution remains highly uncertain, as both sides’ demands remain far apart. To account for this uncertainty, we outline three scenarios, differentiated mainly by energy and agricultural price paths and the size of the global confidence shock, which together drive economic outcomes and policy responses.

The three scenarios are (see Figure 3):

- Gradual reopening: The truce evolves into lasting peace, with the Strait gradually reopening during April and early May. We assume that oil, gas and agricultural raw material prices peak in Q2 and return to their pre-war levels by the end of the year. To model a global confidence shock we increase the investment premium by 0.5 percent with elevation lingering until mid-2027 due to the elevated uncertainty and caution.

- Prolonged disruption: The ceasefire fails initially, with ongoing closure of the Strait and additional infrastructure damage. A more durable agreement is reached later in Q2, allowing gradual reopening of the Strait. We assume oil, gas and agricultural raw material prices peak in Q2 and return to their pre-war levels in the second half of 2027 and that the investment premium rises by 1 percent until mid-2027.

- Permanent disruption: The conflict escalates into a broader war, including attacks on regional energy infrastructure and possible US ground involvement. Although hostilities end late in the year, Iranian control of the Strait persists, and normal flows resume only gradually during 2027. We assume oil, gas and agricultural raw materials prices peak in Q4 2026, while the investment premium rises permanently by 3 percent.

In the remainder of this outlook, we discuss the impact on inflation and economic growth in each of the three scenarios.

No region immune to inflationary impact

The supply shock operates through two channels: higher global energy prices as countries compete for limited supply, and the risk of physical shortages. Among advanced economies, Japan is most exposed to potential shortages due to its heavy reliance on Middle Eastern energy. However, its substantial strategic reserves and ability to pay higher prices reduce this risk, meaning the shock will primarily manifest through higher prices rather than rationing for all major advanced economies. Physical shortages are more likely to occur in emerging markets.

When it comes to price developments, oil markets are globally integrated, with regional benchmarks moving closely together, whereas gas markets remain more regional due to transport constraints. In our analysis, global price paths are applied to Europe and Japan. For the US, we assume slightly lower oil prices and limited gas price effects in the milder scenarios, reflecting current benchmark dynamics. In the permanent disruption scenario, global prices also apply to the US.

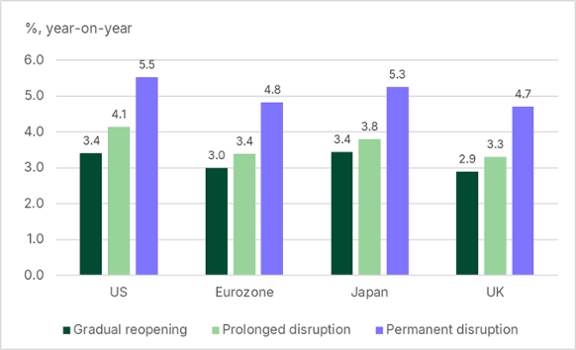

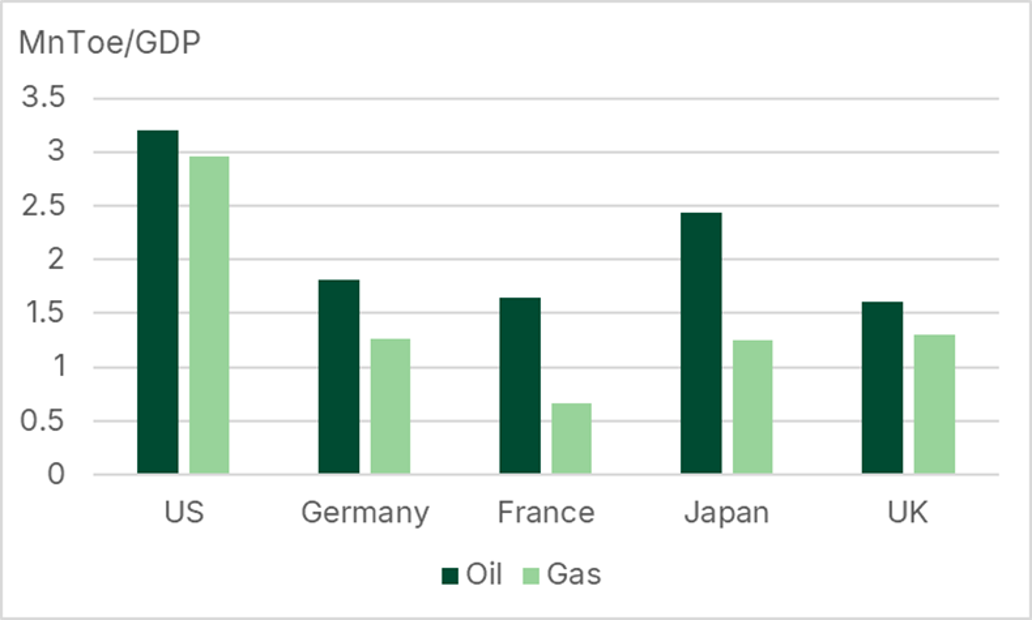

Despite these differences, the inflationary impact of the shock in 2026 is broadly similar across major advanced economies, with differences in headline inflation arising mostly from different pre-war starting positions (see Figure 4). The similar impact partly reflects the relatively high fossil fuel intensity of the US economy (see Figure 5), but also differences in import structures and price transmission. In the US, energy imports, which are dominated by oil, form a relatively large share of total imports (despite it being a net exporter), and domestic prices respond quickly to global changes. In Europe, energy is a smaller share of imports, and price pass-through is somewhat weaker, particularly in the UK. Japan has the highest share of energy in total imports, but its reliance on imported coal and slower price transmission dampen the immediate impact.

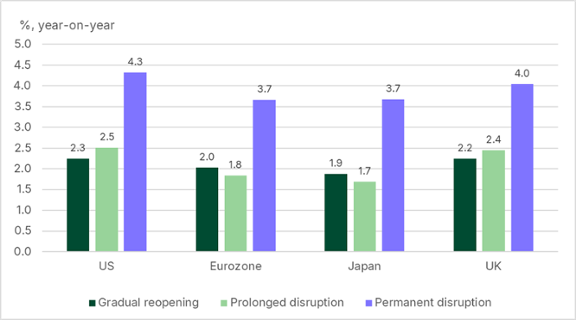

By 2027, inflationary pressures ease significantly in the gradual reopening and prolonged disruption scenarios (see Figure 6). Unlike the 2022 energy crisis following Russia’s invasion of Ukraine, current conditions are less inflationary: excess household savings from the COVID-pandemic period have largely been depleted, reducing demand-driven price pressures that made inflation sticky back then.

Monetary policy also shapes outcomes. In the gradual reopening scenario, central banks largely look through the temporary inflation spike. In the prolonged disruption scenario, the Federal Reserve remains cautious, while the European Central Bank, Bank of England and Bank of Japan implement a limited amount of (additional) rate hikes. For the ECB and BoE, the double-digit inflation caused by the energy crisis in 2022 is still fresh in the memory, which makes them most likely to react. In the permanent disruption scenario, all major central banks respond aggressively when it becomes clear that we are in this scenario.

US growth least impacted, Japan bears the brunt

While inflation effects are broadly similar across advanced economies, growth impacts differ more significantly. In general, we want to emphasise that nowadays fossil fuels are much less important as an input for economic growth than they were during the oil shocks of the 1970s. The number of oil barrels needed to generate 1 unit of GDP has declined by a factor of 15 to 20, due to efficiency gains and substitution (towards renewables and natural gas). Crises in recent years have also taught us that the global economy has become more adaptive than in previous shocks, with companies better able to swiftly adjust global supply chains and households and companies better positioned to withstand shocks due to sizable buffers.

This leaves the terms of trade as the main transmission channel to economic growth. Net energy importers such as the eurozone, the UK and Japan face a deterioration as higher import costs reduce national income. These losses are mirrored by gains for net exporters like the US. However, these gains are partly or fully offset by higher domestic inflation and a negative global confidence shock, which dampens consumption and investment.

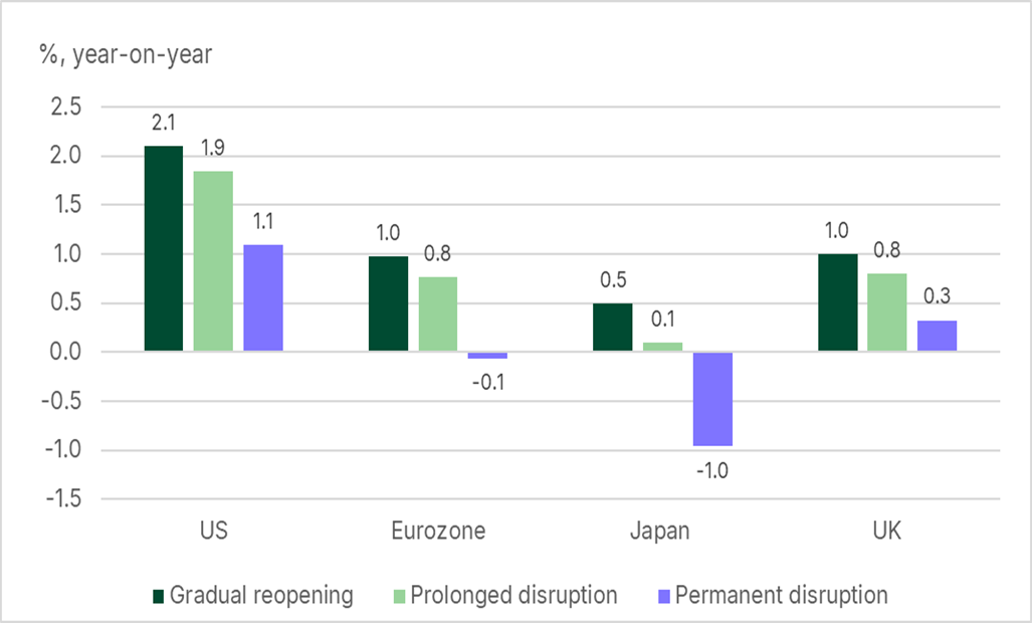

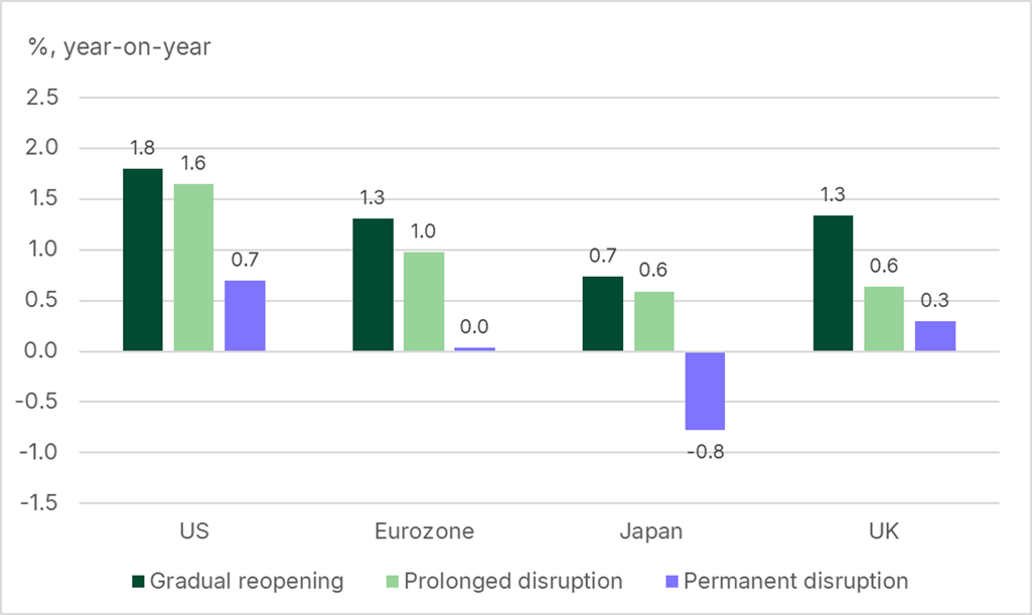

Amongst major advanced economies, Japan experiences the largest negative growth impact across all scenarios, reflecting its high dependence on Middle Eastern energy (see Figures 7 and 8). It is the only major advanced economy to enter recession in the prolonged disruption scenario, while other advanced economies contract only under the permanent disruption scenario. Overall, US growth is least affected, although the impact becomes severe in the permanent disruption scenario.

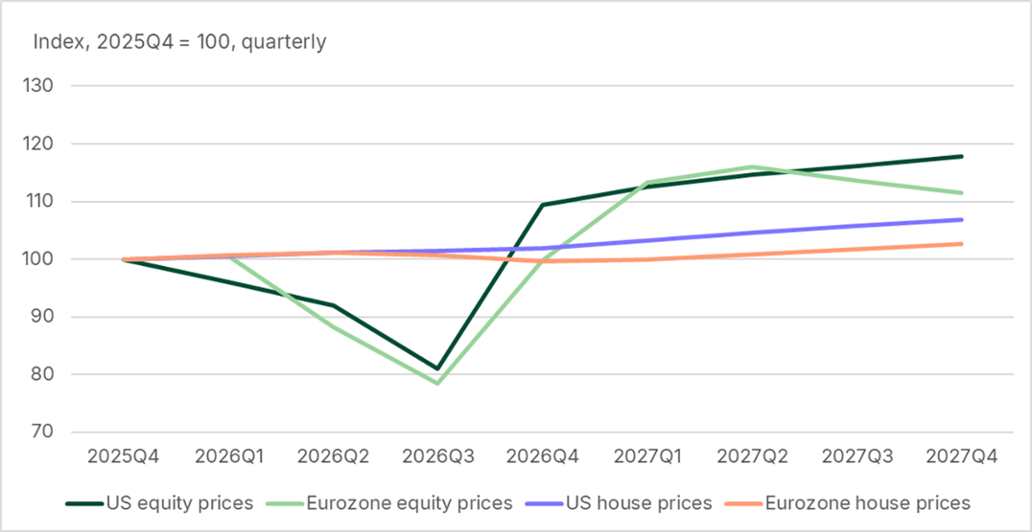

In the permanent disruption scenario, the global confidence shock outweighs any gains from being a net energy exporter. This is particularly relevant for the US, where household wealth is more heavily concentrated in financial assets, which are more sensitive to market volatility caused by such a shock than housing (see Figure 9).

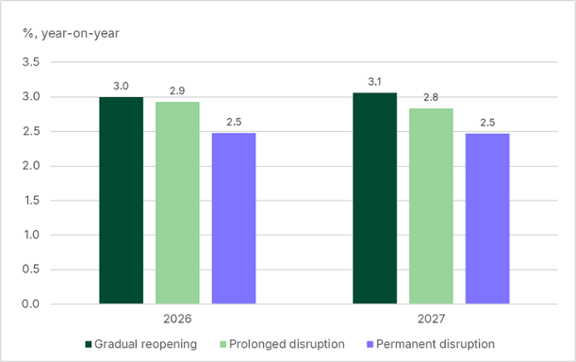

For the global economy, a gradual reopening would have only a minor effect on growth in 2026 and 2027, keeping it broadly in line with the pace of recent years (see Figure 10). Under prolonged disruption, global growth slows modestly, cushioned by fiscal support of around 0.5 percent of GDP. In the permanent disruption scenario, even stronger fiscal measures cannot prevent growth from falling to levels that are by some definitions consistent with a global recession.

European policymakers should not react instinctively

The scenarios suggest that European policymakers should neither underestimate nor overreact to the shock. In the gradual reopening and prolonged disruption scenarios, monetary policy should largely look through the temporary inflation spike. Interest rate hikes are ill-suited to addressing supply-driven inflation and risk undermining investment in the energy transition, which is essential to reducing dependence on imported fossil fuels. The European Central Bank should therefore act cautiously. Controlling second-round effects might be done through fiscal channels such as a windfall profit tax channelled back to those most affected by a loss of purchasing power, as well as clear communication on the temporary nature of the price shock.

If disruption remains contained, fiscal support can remain limited and targeted, focusing on lower-income households that are disproportionately affected by rising energy costs. Broad-based subsidies and any rollback of climate policies should be avoided. As a net energy importer, the eurozone is inherently made poorer by higher energy prices. Attempting to offset these costs through widespread compensation would therefore impose an additional burden on public finances.

Instead, policymakers should address the root cause of the shock for Europeans: dependence on imported fossil fuels. This crisis presents an opportunity to accelerate the energy transition by expanding renewable capacity and reducing demand, including through a strategic shift away from energy-intensive, low-value-added industries. Achieving greater resilience requires accepting that energy may not remain both cheap and abundant during decarbonisation. Policymakers should prioritise protecting vulnerable households and critical sectors in the short term while allowing less future-proof industries to adjust. With industrial policy gaining prominence in the EU, persistently high fossil fuel prices could ultimately serve as a catalyst for structural transformation.