- Emerging markets ended 2025 with a position of relative stability, steady growth and contained inflation; they have now been tested by a fresh global energy shock following the escalating tensions in the Middle East.

- The Strait of Hormuz fallout is impacting countries differently, triggering a wide mix of short- and long-term policy responses. These policy choices will determine if countries perpetuate their fossil fuel dependency or pave the path for alternative sustainable sources.

- Three scenarios are outlined, each reflecting how various levels of blockage in the Strait of Hormuz could affect oil prices and emerging markets’ economies.

- This episode is a reminder of the urgent need for greater resilience through diversified supply chains, robust institutions, as well as an accelerated transition to clean energy to achieve self-sufficiency.

Emerging markets once again tested

In 2025, emerging markets largely succeeded in attracting investor interest due to their relatively stable economic performance. This was evident in their strong currencies led by a weakening US dollar, steady growth, and controlled inflation. Investor optimism was expected to persist into 2026, with emerging markets demonstrating an increased capacity to address ongoing challenges, such as tariffs and interest rate changes in advanced economies.

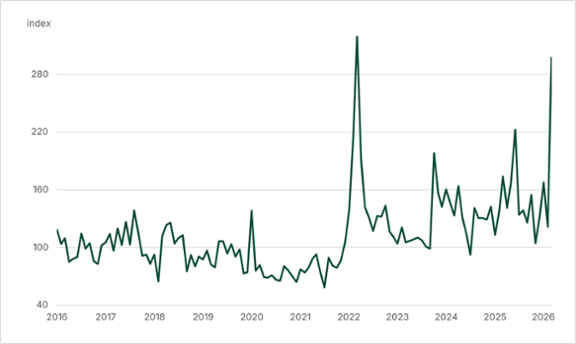

The latest shock, the blockage of the Strait of Hormuz and the destruction of critical energy infrastructure in the Middle East with worldwide repercussions, have brought about an additional layer of instability to emerging markets. Geopolitical risks are once again testing their resilience (Figure 1). Normally, roughly a fifth of global oil and LNG flow through the Strait. The transportation of fertiliser was also impeded and, given the timing of the planting season in certain regions, this disruption has already been affecting some food producers reliant on imported fertilisers.

A two-week ceasefire was announced on April 7, 2026, bringing about some relief to global financial markets as oil flows through the Strait were set to resume. However, after US and Iran failed to reach an agreement, we anticipate a challenging path toward lasting stability in the region.

The lessons from this new shock highlight the urgent need to diversify supply chains, strengthen institutions and accelerate the shift from fossil fuels toward clean energy. Such measures are essential for nations to increase energy security and reduce volatility in capital flows.

Alternative scenarios

The Middle East’s escalating tensions and blockage of the Strait of Hormuz are lasting longer than most initially expected. We outline three possible scenarios of how these events and their consequences might develop; their likelihood depends on how long tensions and disruptions last.

A gradual reopening of the Strait of Hormuz, with shipping picking up to more normal levels towards the end of the year. In this scenario, oil, gas and fertiliser prices are expected to peak in the second quarter of 2026. Brent oil prices already reached USD 118 per barrel on April 7, 2026 (Figure 2) and we expect prices to decline gradually to around USD 75 per barrel towards the end of 2026. We think that even as shipments slowly resume through the Strait, the damage to oil and gas infrastructure may delay a return to normal, while heightened precautionary stockpiling could further boost fossil fuel demand.

Inflation in emerging markets on average could increase to around 4.7% in 2026 from 4.2% in 2025. Meanwhile, GDP growth could slow down to around 3.8% in 2026 from 4.4% in 2025, alongside a decline in activity in sectors most affected by the current events including transport, agriculture exports and tourism. Lastly, we would expect a start to the rebuilding of destroyed infrastructure in the Middle East in the second half of the year.

This manageable scenario of relatively short-lived disruption is captured in our current forecasts. It could temporarily support oil-exporting emerging markets, including Gabon and Nigeria. However, their dependency on fuel imports and how this translates to inflation in these countries may offset some of the positive impact from oil windfall gains. The largest burden would be on oil-importing countries, including India, the Philippines and Vietnam.

The larger emerging economies, including China, are in better positions to weather the repercussions under this scenario, because of their higher fossil fuel inventories, access to other energy sources, including (until recently) from Iran. Additionally, current low inflation in China allows more room for government and central bank support compared to other countries.

Indeed, how emerging markets are affected will largely depend on how much flexibility governments have in their budgets to help households and businesses cope with high energy costs. Central banks are expected to raise interest rates and intervene where possible with foreign reserves to avoid sharp currency weakness across emerging markets.

A prolonged disruption scenario contemplating negotiations muddling through while the Strait blockage is prolonged beyond the second quarter. This will likely result in oil prices of around USD 110 per barrel in the second quarter and gradually declining to USD 80 towards the end of 2026. The prolonged instability is expected to weigh heavily in the emerging markets’ sovereign risk premium, raising the costs of foreign financing. The drag on emerging markets’ growth and inflationary pressure would be prolonged to 2027.

Emerging markets’ GDP growth would decline to around 3.2% in 2026 and inflation would take an even larger hit on average, increasing to 5.2% in 2026. The countries hardest hit would be those with limited oil and gas inventories, that have to buy fossil fuels at considerably higher spot prices. This would include low-income countries in Southeast Asia. Alternative energy sources will urgently be tapped, including prolonging the decision to temporarily lift US sanctions to Russia and increasing even further strategic oil stockpiles. Central banks in emerging markets are expected to act more decisively, under this scenario, to reduce inflation expectations.

A permanent disruption scenario involves a prolonged blockage of the Strait and broader global tensions, with oil prices peaking at USD 150 per barrel in the fourth quarter of 2026 and prices gradually descending throughout 2027, pushing the global economy toward recession. This will lead to severe energy and food shortages – associated with low production and excessive transport costs, as well as low growth and double-digit inflation throughout emerging markets. This is compounded by heightened and broad social unrest. Poverty will increase significantly with rising unemployment and food scarcity. Aggressive monetary policy would lead to a rapid slowdown in emerging markets’ GDP growth, tempering in time, oil demand and prices.

Different stories, different regions: Gulf countries and emerging Asia in focus

The effects of Middle East escalation and the Strait of Hormuz blockade vary by country, based on their economic structure, reliance on fossil fuel and fertiliser imports. Emerging markets’ governments are increasingly implementing mitigating measures, most assuming a short duration of the Middle East escalation, aiming at temporarily offsetting the higher energy and food prices. Some countries, including Mexico are reviving policies that were implemented after Russia’s invasion of Ukraine.

As for central banks in emerging markets, for now, intervention has been focussed on foreign currency markets, to limit the depreciation of their currencies and not on increasing rates to tame inflation. India’s central bank interventions to stabilise the currency have been large. Hence, the spectrum of policy responses is broad.

Latin America, emerging Europe and Africa are expected to remain relatively stable because of the combination of commodity exporting and importing countries. The Middle East and emerging Asia will be more impacted, making policy responses crucial for recovery.

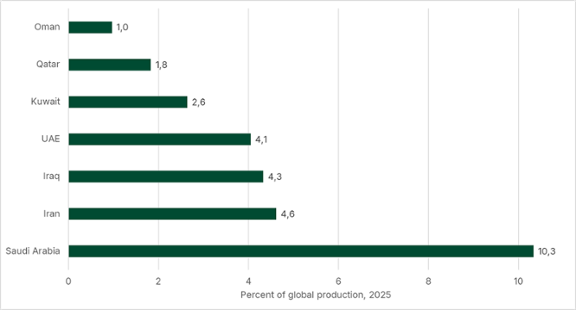

The Gulf countries produce around 30% of the world’s oil (Figure 3). As the epicentre of the conflict, the Middle East countries are suffering most acutely. Investment activities have largely stalled, and the tourism sector has been significantly damaged. Alongside substantial losses to civilian and critical infrastructure, these factors are leading to a reassessment of the risk premium of the countries in the region, including government bond yields. Governments are trying to protect the most vulnerable with broad-based fiscal packages. They are in talks to build new pipelines to complement existing ones and diversify fossil fuel transport routes; this would be a long-term project.

According to the UN Development Programme, the regional economic cost, so far, is estimated to be the largest worldwide, up to 6% of collective GDP. Unemployment is projected to rise by up to 4 percentage points. This is more than double the number of jobs created in 2025, which is expected to lead to a sharp increase in poverty. Migrant workers from countries such as Egypt, Morocco, Jordan, Pakistan and Sri Lanka, who are predominantly employed in the Gulf, face declining incomes. This slowdown in employment will likely result in reduced remittances, which are a vital source of capital flows for their home countries. At the same time, the recovery once reconstruction and oil exports resume should lead to strong growth in the region in 2027.

Emerging Asia, the world’s largest manufacturing hub and net energy importer, is heavily affected due to its reliance on Gulf oil. Crude oil from the Middle East makes up about 60 percent of Asia’s total oil imports. Despite gradual progress in clean energy, Asia remains dependent on fossil fuels. The countries most affected, like the Philippines and Indonesia are those with limited spare oil and gas inventories and no forward contracts, having to pay spot prices for their energy imports. Some countries were prompted to turn to local coal supplies, as seen in India, Indonesia and the Philippines. But coal cannot replace fuel and prices at the pump in these countries surged by up to 60% in a few weeks.

In recent weeks, several emerging Asian governments, constrained by limited fiscal space, have rapidly introduced energy-saving measures. The public administration can work from home in Thailand and Vietnam, while the Philippines has shut down schools. Meanwhile, others widened their budget deficits through increased fuel subsidies. The search for alternative markets has led countries to maximise the use of temporary US exemptions from sanctions on Russia. Some are giving more attention to the energy transition, including Indonesia’s government, who has supported a shift to renewable energy and instructed the replacement of diesel plants with solar plants and battery energy storage.

A threat or opportunity for clean energy

The current energy shock is triggering different choices that will impact the future of the energy transition. First, governments of fossil fuel producing emerging markets are likely to seize the opportunity and increase fossil fuel production. Higher oil prices will likely attract foreign companies seeking high returns by drilling more in Africa and Latin America. In addition, local coal demand could increase further in countries like India and Bangladesh. This could encourage more coal production. Bangladesh is already building up coal-fired plants. These countries are likely to face a delay in their energy transitions.

Second, in some net energy-importing countries, broad subsidies for fossil fuels will be keeping their prices low, making it somewhat harder for clean energy to compete. These subsidies distort markets by making fossil fuels artificially cheaper than renewable options. The pace of the energy transition toward renewables will depend on how long fossil fuel subsidies are held in place.

Third, if governments allow fossil fuel prices to reflect real shortages and provide targeted support for those most in need, renewable energy prices would become even more competitive. Already, the prices of solar panels plummeted by 70% between the start of 2022 and the end of 2025. Emerging markets’ storage demand is also increasing, as the electricity system transitions to renewable energy. With proper market pricing of energy sources and targeted renewable policies as being implemented in Indonesia, this could help improve self-reliance, energy security, and reduce carbon emissions.

Conclusion

A prolonged escalation of the conflict and blockage of the Strait of Hormuz needs to be avoided at all costs. This crisis serves as an impetus for energy diversification and prioritising clean energy. Governments now have the opportunity to send the right policy signals that prioritise energy security.

Countries must move away from energy sources that contribute to environmental harm and encourage concentrated ownership of resources, mostly in the hands of governments. If governments keep returning to fossil fuels through any form of incentives instead of supporting the use of the most sustainable forms of clean energy, they risk perpetuating a cycle of resource dependency and geopolitical tensions.

Decisions made during this crisis will shape emerging markets and the global economy for years.The impact of political risks and wars, caused by poor government choices that hindered global solidarity, democracy, and wellbeing, can no longer be ignored.

Forecast table selected emerging economies

| GDP growth (% yoy) Inflation (CPI, % yoy avg) | |||||||

|---|---|---|---|---|---|---|---|

| Prelim. | Forecast | Prelim. | Forecast | ||||

| 2024 | 2025 | 2026 | 2024 | 2025 | 2026 | ||

| Bolivia | -1,1 | -1,2 | -2,7 | 5,1 | 19,5 | 34,7 | |

| Brazil | 3,4 | 2,3 | 1,7 | 4,4 | 5 | 3,9 | |

| Chile | 2,4 | 2,5 | 2,6 | 3,9 | 4,2 | 3 | |

| China (mainland) | 5 | 5 | 4,5 | 0,2 | 0 | 1,2 | |

| Colombia | 1,5 | 2,6 | 2,3 | 6,6 | 5,1 | 6,1 | |

| Ecuador | -2 | 3,7 | 2,3 | 1,5 | 0,7 | 2,7 | |

| India | 7 | 7,6 | 6,6 | 4,9 | 2,2 | 4,8 | |

| Indonesia | 5 | 5,1 | 5,2 | 2,3 | 1,9 | 3,1 | |

| Ghana | 5,7 | 6 | 5 | 22,9 | 14,2 | 5,8 | |

| Kazakhstan | 5 | 6,5 | 4,4 | 9 | 11,4 | 11,4 | |

| Kenya | 4,7 | 4,7 | 4,5 | 4,5 | 4,1 | 5,9 | |

| Mexico | 1,1 | 0,8 | 1,6 | 4,7 | 3,8 | 3,9 | |

| Pakistan | 3 | 3 | 3,4 | 12,6 | 3,5 | 6,2 | |

| Peru | 3,5 | 3,4 | 3 | 2,4 | 1,5 | 2,5 | |

| Philippines | 5,6 | 4,5 | 4,1 | 3,2 | 1,6 | 4,3 | |

| Poland | 2,9 | 3,5 | 3,7 | 3,7 | 3,6 | 3,3 | |

| Russia | 4,3 | 1 | 1,2 | 8,4 | 8,7 | 6,2 | |

| South Africa | 0,5 | 1,1 | 1,3 | 4,4 | 3,2 | 3,9 | |

| South Korea | 2 | 1 | 2 | 2,3 | 2,1 | 2,1 | |

| Thailand | 2,9 | 2,4 | 1,5 | 0,4 | -0,1 | 0,9 | |

| Turkey | 3,5 | 3,6 | 2,8 | 58,5 | 34,9 | 30,3 | |

| Uzbekistan | 6,5 | 7,7 | 7,1 | 9,6 | 8,8 | 7,4 | |