- Organic farming is less exposed to fertiliser and energy price shocks resulting from the war on Iran, because it avoids synthetic inputs. This could narrow the price gap between organic and conventional food.

- But a smaller price gap does not automatically raise demand. If the conflict pushes up inflation, falling consumer purchasing power could reduce organic food consumption in the short term.

- Over the longer term, the conflict reinforces the case for a more resilient food system, one that depends less on imported fertilisers and fossil energy.

The Hormuz Strait is critical for global commodity flows. On a normal day, about 20% of both global oil and liquefied natural gas passes through it, alongside around 30% of global fertiliser trade, including urea, an important nitrogen fertiliser. The disruption hits the global fertiliser market in two ways: a direct reduced availability of nitrogen fertilisers. and higher production costs, because fertiliser processing is energy-intensive and is therefore being impacted by the sharp rise in fossil fuel prices.

We already see rising fertiliser prices on world markets (Figure 1). If the conflict lasts much longer, the effects could be significant once producers work through existing fertiliser reserves. Fertilisers support the production of food staples, including soybeans and cereals, that are important for food security. While European countries are less directly exposed to fertiliser shortages, integrated global fertiliser markets mean the shock will eventually transmit through fertiliser and food prices across the world.

For Europe, the war is another wake-up-call for energy self-sufficiency, and we should apply the same logic to our food system. Our exposure to global fertiliser markets is making our food chains vulnerable. Shifting to organic farming and improving soil health would provide a meaningful protection against this. Unfortunately, organic food uptake by consumers is hindered by a range of factors, including higher prices than conventional products.

Could a fertiliser supply shock, induced by the escalating Middle East tensions provide a boost to the development of the organic sector? We examine the cost structure of organic production and how consumers may respond to relative price changes, using insights from the gas price rises induced by the Ukraine crisis.

The Iran war could contribute to closing the organic premium

The Iran war affects the cost structures of conventional and organic farming differently. Because organic crop farmers do not use synthetic fertilisers like urea, they are more insulated from the input price shocks currently affecting global commodity markets. Organic and regenerative farmers have invested in alternative routes for fertilisation such as manure, nitrogen-fixing plants and soil health practices, and therefore do not suffer from rising fertiliser and fossil fuel prices to the same extent.

A 2024 study among 30 conventional and 30 organic farms, both arable and dairy, found that organic farms have around 50% lower total energy inputs in their production on average compared to conventional operations. Organic arable farms did use roughly 10% more diesel, as e.g., mechanical weeding replaces chemical weed control, but the absence of energy-intensive mineral nitrogen fertiliser and synthetic pesticides more than compensated for this. Organic dairy farms used less diesel than their conventional counterparts in the study.

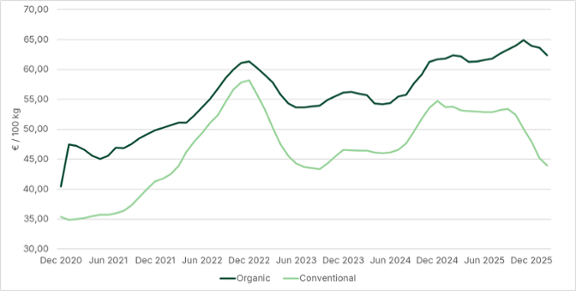

Both the energy and fertiliser price rises in response to the Ukraine war and Russian sanctions offered a view of these dynamics at play. As gas prices surged, fertiliser and feed costs rose more for conventional dairy farmers, the price premium for organic milk narrowed significantly in 2022 in Europe. A similar pattern emerged for products like organic tomatoes in the Netherlands, albeit not for some other product pairs such as apples or potatoes, which shows the complex interplay of factors determining ultimate food prices.

One caveat is that organic farmers are not always independent from conventional inputs with a closed nutrient cycle. For example, in the Netherlands, organic guidelines permit organic livestock farmers to use up to 30% of nitrogen fertiliser from conventional manure in line with EU regulation. This is itself produced by livestock eating conventional feed, likely produced with synthetic fertilisers.

Inflation brings headwinds to organic consumption

So far, we have looked at production costs. But food markets are also shaped just as much by what people can afford. From the supply side, organic food could become more affordable relative to non-organic substitutes. However, that does not automatically mean the organic market share will increase. Relative price is just one of the aspects driving consumption decisions.

A countervailing and potentially overruling factor in the short-term is inflation. The war on Iran represents a supply shock for oil, gas, fertiliser and petrochemical derivatives. This supply disruption is already pushing prices higher. Global oil prices, for example, have risen from below 70 dollars per barrel to around 100 dollars per barrel currently.

It is uncertain how the war will unfold. In the most positive scenario, trade through the Strait of Hormuz will resume quickly. Even in this scenario, we expect a mild uptick in inflation due to the supply disruption already suffered as well as damage and delays to production facilities. In a more negative scenario in which the war reignites and traffic through the Strait takes much longer to resume fully, inflation could be higher for longer.

This supply-driven inflation would hurt purchasing power for European consumers, which could mean they cut expenses. Since organic food in general is more expensive than non-organic substitutes, these effects could lower demand for organic foods in the short run.

This is consistent with the dynamic in the Ukraine war crisis. Despite rising gas and synthetic fertiliser prices, organic consumption on average fell across the EU for the first time. It took until 2024 for the euros spent per capita on organic food to eclipse the amount of 2021, without considering inflation. A loss in purchasing power implies a dampening effect on organic sales. Here, too, the impact on individual producers depends on their exact business model. For example, producers with direct-to-consumer models may prove more resilient.

Short term and long-term lessons

In the short term, organic food production is less dependent on inputs that pass through the Strait of Hormuz than conventional food production. This reduces exposure to fertiliser and energy supply disruptions and can help narrow the price gap between some organic and conventional products. However, this cost benefit will likely be partly offset, or even outweighed, by the increased inflation and associated loss in purchasing power following the war.

In the longer term, the effects of the war are an argument to accelerate the adoption of organic agriculture and healthy soil practices. The war on Iran provides the same lesson to policymakers as the war on Ukraine: becoming resilient in the face of a geopolitically turbulent world, reducing our dependencies on foreign inputs and fertiliser markets makes strategic sense.

Building resilience does not just mean creating stockpiles of fertiliser, it also means growing our food on healthier soils that require fewer synthetic inputs, making use of organic manure, using nitrogen-fixing plants and starting discussions on the reuse of nutrients in wastewater.

Organic and regenerative farming is not just better for human health and the environment; it may also help Europe to stay resilient against geopolitical shocks. Policymakers would do well to take note.