- Capital allocation is central to transitions, shaping both the build-up of sustainable practices and the phase-out of unsustainable ones. We know that financial markets on their own will not mobilise capital at the scale and pace required for transitions, while the current policy approach of pricing externalities and mandatory disclosure regimes remains insufficient.

- In Europe today, plenty of policies influence the allocation of capital, yet there is no deliberate framework for financial guidance that coordinates capital flows in line with public objectives.

- Many instruments can and have been used to guide finance. This range includes subsidies in the real economy alongside credit guarantees, cheaper policy rates for specific collateral and maximum ceilings or minimum quotas for financing to specific sectors.

- To support sustainable economic development, we Europe needs a comprehensive framework of financial guidance. We can build on a wealth of historical experience with financial guidance regimes as well as contemporary examples from around the world.

Our societies and economies are in urgent need of restructuring to stop us from exploiting the planet and safeguard its livability. There is no singular solution that will get us to a truly regenerative economy and the transition contains many uncertainties. What is certain, however, is that we cannot transform our society without considering the allocation of capital. Capital conditions determine which economic activities can scale and which need to wind down. Whilst such capital allocation decisions are currently also influenced by financial policy (through tax breaks for sustainable investment purposes or a public guarantee to enhance home ownership for example) there is no overarching framework that deliberately guides financial flows. In this article, we argue that what is missing in Europe is not policies that influence finance in general, but rather policies that aim to consciously guide finance in line with public goals.

As part of the transitions ahead, capital will be needed to scale up sustainable solutions. And more importantly perhaps, capital needs to be redirected away from activities that reinforce unsustainable practices, such as the fossil fuel industry and unsustainable agriculture. Access to capital from financial institutions is necessary for companies to be able to expand or continue their activities, beyond their own revenues and assets.

Financial markets are not designed to facilitate long-term transformations

In principle, financial institutions make lending and investment decisions based on risk-return assessments. At this point, only a small fraction of financial decisions globally are driven by impact considerations. As a result, the allocation of capital on a macro-economic level is largely driven by short-term profitability.

Investments that maximize profits do not necessarily facilitate long-term transformations. Take forests as an example. Financing a company that generates immediate profits by cutting down the forest to sell timber or convert the land to agriculture is profitable. By contrast, leaving the forest and its public benefits (such as carbon storage and biodiversity protection) intact, won’t be reflected in any company’s revenues. From a purely profit-maximising view, financing harmful activities therefore remains attractive in the short term.

One might wonder why private finance does not effectively account for long-term risks such as climate change and biodiversity loss. These will ultimately erode the base of our economies, and as such, should present serious financial risks. Yet these risks tend to be longer term than investment horizons and difficult or impossible to quantify, let alone monetize. Moreover, the damages to the environment or public health will be borne by society at large, rather than by those causing or financing harm. As a result, these costs will not appear on investors’ balance sheets and have little influence on their allocation decisions while financial return remains the primary objective.

Positive effects contributing to long-term societal value don't necessarily fit the balance sheet either. It is similarly challenging to monetise the added value of increased social cohesion, of lower CO2 emissions through more renewable energy supply, or of increased wellbeing as a result of higher quality healthcare, for example. As a result, private finance will not only overfinance harm, but also underfinance these non-monetary virtues.

This explains why investment for sustainable development remains insufficient, whilst harmful practices continue. The sustainable “investment gap” is estimated to be $4 trillion annually. Moreover, the UNEP State of Finance for Nature report shows that for every dollar invested in protecting nature today $30 USD are spent destroying it.

Why there is no ‘quick fix’ in markets

Solutions such as pricing externalities and disclosure regimes can improve the functioning of market, but these policies alone are unlikely to redirect financial flows at the scale and pace required for systemic transformation. Take for example CO2: determining an appropriate price on carbon remains highly contested and is subject to considerable uncertainty. This generally results in prices that are too low to fundamentally alter investment decisions. Similarly, disclosure regimes have led to more transparency about the impact of investments but does not come with any obligation for investors to change their allocation decisions. All the while, the general principle of capital allocation solely based on profit maximization remains unchallenged.

Finally, a system-wide transformation requires coordinating financial flows across multiple complementary sectors. The transition to renewable energy requires fossil phase-out as well as investment in wind farms or solar parks and in storage and the grid. The latter are interdependent: the value of investment in solar parks is conditional on the existence of the appropriate grid and vice versa. Specific pricing alone cannot guarantee that various investments necessary for the transition occur simultaneously across sectors. Thus, coordinating financial flows to target economic development at the source is an essential complement to pricing and disclosure policy.

Forms of financial guidance

Credit and investment guidance, includes all policies meant to influence the allocation of credit and/or investment. We include both credit and investment because this captures most private financial flows. While (bank) credit remains a dominant form of company financing, investments also represent a significant share of company financing. Therefore, a holistic financial policy should aim to guide both credit and investment. Guidance regimes can be designed by democratically elected local, national or supranational bodies and implemented by both (national) governmental organisations and central banks.

Credit guidance policies are scarce in Europe nowadays, although some policies that aim to influence financial allocation decisions exist. In the Netherlands for example, there is a ban on financing cluster munition, enforced through the financial markets supervisor. We also have softer, promotional measures that aim to influence financial allocation decisions, such as the National Mortgage Guarantee scheme (NHG in Dutch). Through this guarantee, the government derisks mortgages on homes beneath a certain maximum price. The idea is that this will incentivize banks to lend to potential borrowers more freely, which is ultimately thought to contribute to extending homeownership among the population. Together with the mortgage interest deductible from Dutch income tax, these two instruments provide powerful incentives for higher mortgage debt in the Netherlands. As of now, the Dutch government also provides tax breaks for sustainable investments through the Regeling Groenprojecten. This facility is meant to attract capital for innovative projects contributing to specific goals such as the circular economy, sustainable agriculture, climate adaptation and renewable energy. These are all forms of guidance. Moreover, from supervisory capital requirements for banks to the subsidies that governments disburse in the real economy and, arguably, to those elements of competition law that matter to a business bottom-line: the allocation decisions made by private finance are profoundly affected by government policies.

Yet we have no evidence of any government, central bank or ministry of finance in Europe that will claim it is substantially guiding finance as a whole. Instead, the belief that capital markets, if optimised for efficiency, will address the challenges ahead of us is dominant. The European Commissions Capital Markets Union fact sheet (2020), clearly exemplifies this approach stating: “Efficient capital markets will contribute to channeling funds to the twin Green and Digital transition, and capital markets will help address societal challenges.”

A rich history of financial guidance

In the past, credit guidance policies played an important role in Europe. Between 1945 and the early 1980’s – the period of the reconstruction after WWII, rapid economic expansion in the 1960’s and eventually oil price shocks and recession in the 1970’s – multiple governments including France, Germany, Italy and Belgium explicitly aimed to guide finance. Moreover, at that time central banks were still largely under control of the Ministry of Finance. As such all the relevant policies for guiding finance could be coordinated.

In France, this coordination was done in the Conseil National du Credit (CNC), to promote sectors such as public transport or export industries. While the finance minister was formally the president, his credit council was in practice dominated by the Banque de France. The CNC instituted comprehensive guidance, using special arrangements with nationalized savings institutions to promote priorities while aggregate credit ceillings were used to help manage inflation, with exemptions for some priority sectors such as agriculture, export-oriented manufacturing, railway transport and electricity supply. In limited cases, they also intervened with direct ceilings or quotas for specific businesses or sectors (such as a stop on lending to large chicken farmers, p. 226), but this was rare. Mostly, guidance left some space for banks to make decisions. Financial guidance policies helped public actors give direction to great economic development.

Outside of Europe, the East Asian Tigers have notably employed credit guidance during their economic boom, to scale strategic sectors such as export-oriented manufacturing. Even the International Monetary Fund, at the time quite known to be critical of too much state interference, concluded this was effective. China employs a form of credit guidance today with both public banks and government guidance funds. These government guidance funds, generally owned by a branch of government and state-owned enterprises, mobilise risk capital for both start-ups and scale-ups in strategic priorities on a large scale. While this design is probably irreproducible outside China, it does show that a coordinated approach across various policy fields can be effective.

Note that while all policies discussed above guide finance, they do not imply complete centralised economic planning. Rather, these policies help set the guardrails and direction within which decentralized markets can operate.

Various instruments to implement financial guidance

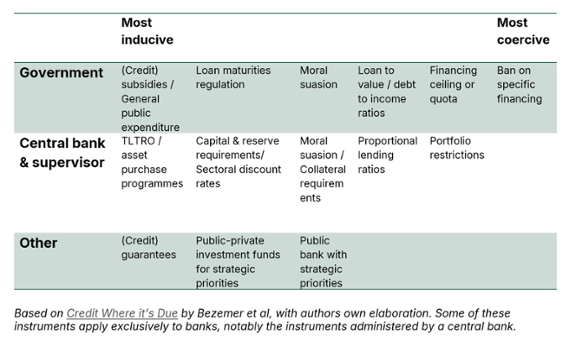

Governments have used a very broad range of instruments to implement financial guidance, some of which we have explained above. An overview of guidance instruments can be found in table 1.

Credit guidance instruments vary in at least three important dimensions. The first is demand-supply (demand is italicized in Table 1). Credit demand is targeted through, for example, loan to value ratios, debt to income ratios, loan maturities regulation and credit subsidies. Many of these tools are still present on housing markets. In the Netherlands, for example, a 100% loan-to-value limit constrains how much people can borrow for their house, as does a debt-to-income ratio. Furthermore, the loan maturities regulation sets a limit to the duration of a mortgage (usually no longer than 30 years). In other countries, credit subsidies have been used to increase home ownership, but also to boost credit to export-oriented industries and to farmers.

On the credit supply side, many instruments exist, some of which have been used recently. The ban on financing cluster munition was introduced in the Netherlands in 2013 is a clear example. Across the EU, Public banks and credit guarantee programmes are active in targeting public priorities, by guaranteeing credit to the cultural and creative sectors for example. In the last decades central banks also employed Targeted Long-Term Refinancing Operations with the aim of stimulating banks to lend to companies and households. Some other finance guidance instruments that influence credit supply, such as capital and reserve requirements, are part of supervisory requirements in the EU currently. While these influence credit, they are not currently used to deliberately guide it. India provides a good example of proportional lending ratios, with banks required to engage in a minimum % of lending to priority sectors.

The second dimension of financial guidance instruments is the range from inducive to coercive guidance. For example, in the case of the energy transition, a government could decide to offer a TLTRO with a lower interest rate for renewable energy financing. This would be inducive; banks are in no way forced to make use of the facility. If a central bank would instead lower capital requirements for renewable energy, and increase them for fossil fuel lending, this would be more coercive: all banks are subjected to the rules, although banks are still allowed to choose. An outright credit ceiling on fossil fuel financing would be more coercive, and a ban would leave financiers no choice.

The last dimension concerns the implementing actor. Subsidies can come directly from a ministry or central government. Credit guarantees are currently often administered through the European Investment Bank in the EU, and TLTRO’s come from the central bank. Meanwhile portfolio restrictions and capital requirements are administered by financial supervisors, which in most countries are also the central bank.

All in all, this wide spectrum of credit guidance instruments makes it possible to develop and refine a credit guidance regime that best fits the institutional setup and public aim in question. For stimulating a certain type of credit with high societal value, such as the cultural and creative sectors or renewable energy, an inducive instrument might fit well. This could be done through credit guarantees or TLTRO’s, for example. Yet, arguably, in cases where direct harm needs to be prevented, a more coercive instrument is more fitting. Developing new fossil fuel projects at this point, for example, undermines our commitment to limit global warming to 1.5 degrees. In this case, an outright ban on financing fossil fuel expansion would fit the goal.

Time to bring back financial guidance in Europe

Capital allocation is central to transitions, shaping both the build-up of sustainable practices and the phase-out of unsustainable ones. In Europe today, plenty of policies influence the allocation of capital, yet there is no deliberate framework for financial guidance that coordinates capital flows in line with public objectives. We know that financial markets on their own will not mobilise capital at the scale and pace required transitions, while the current policy approach of pricing externalities and mandatory disclosure regimes remains insufficient. To support sustainable economic development, we should develop a comprehensive framework of financial guidance. In doing so, we can build on a wealth of historical experience with financial guidance regimes as well as contemporary examples from around the world and choose appropriate instruments accordingly. If we are serious about the sustainability challenges ahead of us, we must take an active role in directing capital flows accordingly.