- In the short term this war will lead to higher inflation and lower economic activity for most major economies, with potentially painful social consequences and difficult trade-offs for central banks.

- A policy reaction that combines protecting people from the harmful social consequences while leaving less desirable, energy-intensive industries exposed to rising prices could speed up the transition to a more just and sustainable economy in the medium term.

How the war affects economies

Analysing the economic consequences from the Iran War starts in the 50-kilometre wide Strait of Hormuz. About 20 million barrels of oil and gas - about 20% of both global oil¹ and liquified natural gas (LNG)² production - normally transit the fifty kilometre wide sea strait each day. Most of this traffic is currently blocked, with no real alternatives for transporting these quantities. Full compensation from strategic reserves (about three months of global oil consumption) is also impossible, so this constitutes an energy supply shock.

Along with oil and gas as the primary affected goods, petrochemical derivatives will be affected as well, including notably fertilizer. Producing synthetic fertilizer is energy intensive, meaning that production facilities elsewhere will be affected by the oil and gas shock, while the Gulf region is a major producer in its own right too, with about 30% of global fertilizer trade³ usually transiting the strait.

So how do these supply shocks actually transmit to economies? This breaks apart into acute supply shortages in some regions, with prices being affected to some degree across the globe. The region bearing the brunt of the direct economic impact is Asia. Asian economies normally import over 80% of the shipments coming through the strait for both oil⁴ and gas.⁵ On prices, the usual references for global oil prices, Brent and WTI, have risen significantly from below $60 per barrel of oil just before the war to about $100 per barrel currently.

However, Asian indices such as the Dubai and Oman oil prices have risen to well over $150 per barrel of oil already. This shows how in the short term Asian economies are more heavily affected by higher prices and in some cases acute shortages. While most Asian economies have some emergency reserves⁶ on hand, some countries are already running out. This is visible through local prices rising sharply in some countries to levels that are prohibitively high for some users, in this way reducing demand.

How financial markets have reacted

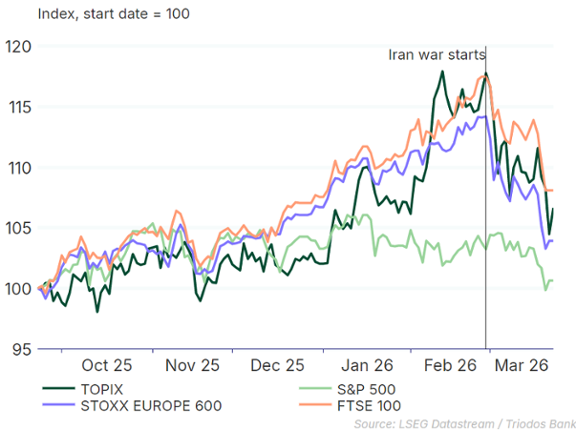

Financial markets have been shaken up by the war on Iran. Equity markets mostly sold off in the first days of the conflict (Figure 1), stabilising somewhat in euro terms for the next two weeks and then falling again as an end to the war became more elusive. US equity markets have been most immune, with some dollar appreciation supporting valuations in euro terms. Within equities, many sectors have been negatively affected including industrials, materials, consumer staples and airlines as well as the interest sensitive real estate and financial services sectors. The main exception to the downward trend were oil majors, moving up somewhat.

Figure 1: Equities in Eur

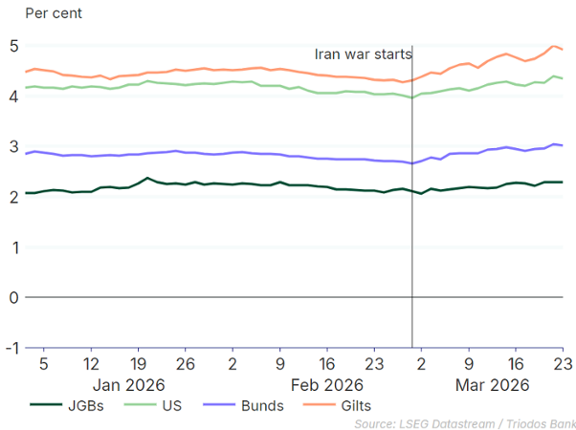

Global bond markets have reacted not so much in one big bang, but through consecutive bouts of volatility as the war spread across the region, making a quick end increasingly unlikely. 10-year yields across the board have gone up significantly for major economies (Figure 2), with additionally spreads increasing for less creditworthy European sovereigns. We see short-term yields rising even more strongly, as markets are reassessing their expectations for inflation and central banks' rate paths upwardly. 2Y yields are up markedly in a bear-flattening of the yield curve, and markets now on average expect both the ECB and the Bank of England to hike rates going forward. The upward move in yields is especially pronounced in the UK, where inflation is still elevated from the last energy supply shock.

Figure 2: Ten year government bond yields

Mostly losers, some winners

It is clear that on an aggregate level this war is an economic cost. Less supply and volatility both mean a negative shock for the global economy. Yet, not everyone suffers. Fossil fuel producers that can still export, most notably, are profiting from higher prices. This includes both Russian and some US fossil fuel producers, as well as fertilizer producers who do not rely on Gulf exports. Perhaps paradoxically, but in so far as demand for oil and gas is lowered, aggregate greenhouse gas emissions might also come down.

Potential future developments

Liquid gas production facilities are quite hard to restart even when the war ends. This is not just due to reparations of destroyed plants, but also repressurizing fields and repowering the installations used to cool gas to a liquid state. This means that even when the Strait of Hormuz reopens, supply will lag its previous level for at least a few weeks. Oil production will likely be somewhat quicker to resume, albeit also with a lag.

While the war lasts, we expect oil and gas prices to become more closely aligned globally. This means rising prices for oil and (liquid) gas in advanced economies compared to current levels. These developments are likely to provide upward pressure to inflation across major economies, especially in Asia, then Europe, then the US through energy costs first and all other product categories second.

While Europe usually imports only 5% of the crude oil and 13% of the LNG traffic that passes through the Strait, it is a major energy importer and therefore exposed to rising prices on world markets.⁷ A prolonged war would also imply fertilizer shortages, which in addition to the humanitarian consequences of disappointing harvests in fall, could drive inflation up further.

Economic activity will be negatively affected, most so in Asia and Europe and to a lesser extent the US. Energy intensive and petrochemical dependent industries, including semiconductor manufacturers, could also suffer from higher input prices as well as shortages. This could subdue last year's growth engine, the investment boom in Artificial Intelligence (AI) and related industries and affect equity markets too, given the stretched valuations in AI- and tech-related stocks.

All in all, a lasting war could imply stagflation for both the eurozone and the UK. Stagflation refers to a situation of stagnating economic activity combined with inflation. Given the levels of economic inequality present in our societies today, this could worsen the cost-of-living crisis for those in the lower part of the income- and wealth distribution, whilst at the same time putting pressure on government budgets.

Policy implications

Central banks will be hard-pressed to decide what to do. They waited out the Russian energy shock first, then raised rates significantly as inflation surged, but found the expected monetary transmission channels wanting. It is unclear what conclusions central bankers have drawn from this episode as of yet.

Traditionally, we expect central banks to hike rates when inflation rises, as currently priced in by financial markets. But given a supply shock, rate hikes might well prove ineffective at reducing inflation. In our current growth-dependent economies, rate hikes can only be truly effective in controlling supply-driven inflation by reducing demand significantly, which would have to happen through socially painful mechanisms such as rising unemployment.

Central banks might still choose to hike rates, if only to anchor inflation expectations and limit the knock-on effects of higher energy and food prices, but this would mean accepting elevated inflation in the near-term. Especially for the Bank of England, with a dual mandate on inflation and growth and in an already softening labour market, this could present a difficult trade-off.

A form of monetary-fiscal coordination⁸ might well be more effective in the short-term to shelter designated parts of the economy from the impacts of the war with more benign social consequences. While we cannot prevent global supply from contracting, we could stem (local) consumer price increases by reducing demand from specific sectors.

This is the lesson that some European government seemed to be learning during the gas price crisis of 2021-2022. After mostly untargeted fiscal stimulus through energy price reductions and income support, working against restrictive monetary policy, some countries rolled back energy price support to some industrial users in an effort to reduce demand. All in all, the crisis lowered European gas consumption significantly.⁹ If done right, such a targeted industrial policy approach could have long-term benefits, too.

After the war on Ukraine, the war on Iran again presents Europe with an energy supply shock. The crucial lesson to draw from both is that the path to long-term resilience is energy independence. Doing so requires both building up renewable energy capacity and lowering energy demand by letting go of the lower value added, energy-dependent industries strategically. This will require policymakers to let go of the idea that energy can remain both cheap and abundant¹⁰ while decarbonizing, and plan for a lower energy but high wellbeing economy instead. Sheltering vulnerable citizens and key industries from the impact of price rises in the short-term while leaving less futureproof industries exposed could accelerate this transition markedly. With industrial policy resurgent in the EU, the unfortunate situation of world prices for fossil fuels and related products rising significantly might be an opportunity for our economies to transform.

Endnotes

1. U.S. Energy Information Administration. (2025). Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint. https://www.eia.gov/todayinenergy/detail.php?id=65504

2. U.S. Energy Information Administration. (2025). About one-fifth of global liquefied natural gas trade flows through the Strait of Hormuz. https://www.eia.gov/todayinenergy/detail.php?id=65584

3. Kpler. (2025). Global fertiliser dependency on Gulf exports: what if Hormuz is disrupted? Global fertiliser dependency on Gulf exports: what if Hormuz is disrupted? | Kpler - Jun 18, 2025

4. U.S. Energy Information Administration. (2025). Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint. https://www.eia.gov/todayinenergy/detail.php?id=65504

5. U.S. Energy Information Administration. (2025). About one-fifth of global liquefied natural gas trade flows through the Strait of Hormuz. https://www.eia.gov/todayinenergy/detail.php?id=65584

6. Asia Media Centre. (2024). The Hormuz buffer: Asian oil security amid prolonged Middle East conflict. https://www.asiamediacentre.org.nz/the-hormuz-buffer-asian-oil-security-amid-prolonged-middle-east-conflict

7. UNCTAD. (2026). Strait of Hormuz Disruptions, implications for global trade and development. Strait of Hormuz disruptions.

8. New Economics Foundation. (2025). A coordinated macroeconomic framework for Europe. https://neweconomics.org/2025/06/a-coordinated-macroeconomic-framework-for-europe

9. Eurostat. (2023). EU gas consumption decreased by 19%. EU gas consumption decreased by 19% - News articles - Eurostat

10. European Commission. (2024). The future of European competitiveness: A competitiveness strategy for Europe (The Draghi Report). https://commission.europa.eu/document/download/97e481fd-2dc3-412d-be4c-f152a8232961_en