- This article explores how banks and financiers can move beyond traditional ESG scoring and exclusionary practices to actively support companies that are reshaping industries from the ground up.

- By identifying and funding mission-driven businesses with deep, innovative, and collaborative potential, financial institutions can become catalysts for transformations.

- Drawing on transition studies and practical frameworks, we reveal how banks can kickstart and push forward the transformations we need.

Most sustainable finance is built around a simple question: is this company responsible enough to lend to or invest in? Banks and asset managers may look at how a company manages its carbon emissions, how it treats its workers, and if the board is diverse enough. Although such ESG frameworks have become more sophisticated, the underlying logic remains the same: assess what a company is doing today, score it against a set of criteria, and allocate capital. More advanced investors may also engage with their investees to encourage them to more responsible practice through active ownership.

While rooted in the right ethics, we can no longer rely on the theory-of-change of ESG and impact investing of scoring, weighing, engaging and excluding. A recent study estimated that even if asset managers representing 80% of investable wealth were to exclude polluting firms, those firms' cost of capital would rise by only around 1%.¹

If we want to solve big challenges like climate change, rising inequality or the rapid loss of natural habitats, we need more than companies that are slightly less harmful than before. We need system transformations.² Exclusion sends a signal, but it cannot drive systemic change on its own. Active ownership practices may help, but financial institutions should go further: not just withdrawing capital from harmful companies but actively directing it toward companies that are changing the systems that cause these problems in the first place.

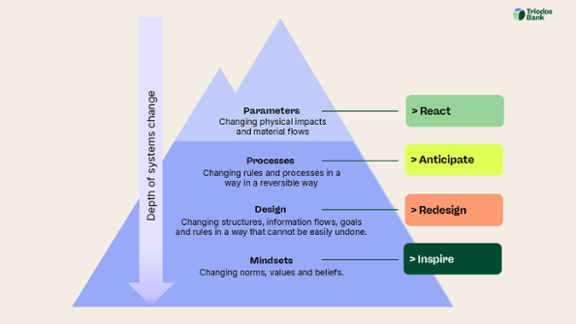

The iceberg of solutions

Not all positive changes are the same. It helps to think about different levels of change, from shallow to deep on the iceberg model. These different levels of change provide insights on leverage points for systems change.³ ⁴

At the shallowest level there are parameters: small, practical improvements. A bakery switching to organic flour, a logistics company replacing diesel with biodiesel, or a building owner adding insulation strips to a property are all examples. These changes are real and measurable, but they are also easy to make and easy to undo.

One level deeper are changes in how a business operates: processes. A farm that starts selling directly to local customers through a weekly subscription box, or a building company that changes its purchasing rules to only biobased materials is doing something significant. These changes affect the relationships and processes of the business, not just one or two numbers in its impact report. However, they can still be undone relatively easily.

Even deeper are changes that restructure how a business fundamentally works: the design. For example, these are farmers who convert their entire operation to regenerative organic agriculture, a fashion company that stops producing seasonal collections and only makes clothes when customers order them, or a steel smelter that replaces a coal furnace with a green hydrogen system.

And at the deepest level are changes in values and beliefs: the mindset. A business owner who genuinely believes that a company cannot be successful in the long term if it damages the natural world, is thinking in a fundamentally different way. This kind of change is the hardest to measure, but it often drives all the other changes and is the most difficult to reverse.

Most companies with good ESG scores are only making changes at the first two levels. Real transformation happens at deeper levels.

Transformation is the scaling of change

Sometimes transformation comes from small, new companies with radical ideas. Smaller players in the niche can lead the way, developing new approaches that larger companies later adopt during certain windows-of-opportunity. The technology that made working from home easy already existed before the COVID-19 pandemic, but it was only when millions of people were forced to use it that it became normal. Heat pumps were a small niche product until rising gas prices and energy security concerns pushed them into the mainstream.

Companies of any size can be transformative, but scalability helps. A community credit union that changes how an underserved population accesses capital can be just as transformative as the fintech startup building the platform that powers it. What matters is not how big a company is, but how deeply it is changing the way its sector works, and how far that change can potentially spread. To finance transformation, banks should look for companies whose way of doing business challenges the norms of their industry, and who have a realistic path to influencing how that industry develops.

What a transformative company looks like

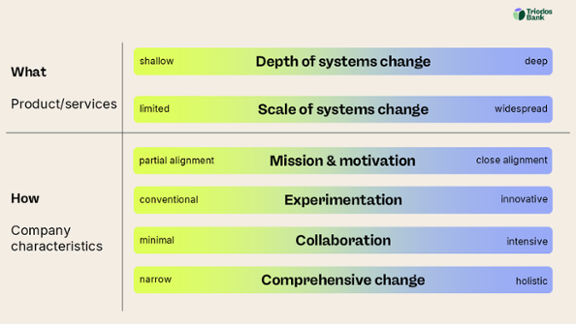

We cannot evaluate how a company may spearhead a transformation by reading the tea leaves, because societal transformations can be unpredictable and impact may be indirect and delayed. This makes it hard to draw a direct causal relationship. Instead, we can try to identify whether a company has transformative potential. To do this, it helps us to look at both what the company does and how it does it.

On the what side, two things matter. First is depth on the iceberg model: does the company's product or service challenge the way its industry works, or does it just offer a slightly better version of what already exists? Second is scale: how many people, sectors, or places could be affected by what this company does?

On the how side, four aspects can inform a transformative evaluation. First, what is the company's core mission and what is its leadership’s motivation? A woodworking business with an entrepreneur that integrates his belief in biobased material across his company and actively campaigns for changes to building regulations is fundamentally different from one that only offers one reclaimed wood product alongside its usual range.

Second, is the company experimenting and learning?⁶ A small urban farm that is testing new growing techniques for shade-grown aromatic herbs, or a local energy project that is trying out new ways for communities to own and manage their own power supply, is contributing to a wider process of change, not just improving its own business.

Third, does the company collaborate with others to spread new ideas?⁷ A food producer that helps set up a regional cooperative, or a consortium of shipping companies that commits to collaborative learning about the use of ammonia as shipping fuel, is shifting the norms of a whole sector. A large group of biodiversity researchers found that transformative change is almost never the result of a single actor working alone. Across 391 case studies, initiatives involving more diverse coalitions of actors, like communities, governments, businesses, scientists and Indigenous Peoples, achieved better outcomes for both nature and people.⁸

Fourth, is the company changing all of itself comprehensively, or just part of itself?⁹ For larger companies especially, it is important to ask whether they are phasing out their harmful activities, not just adding sustainable ones. A company that launches a green product range while leaving the rest of its harmful business unchanged is not really transforming.

These six dimensions together can give financiers a starting point for assessing the transformative potential of organisations.

Turning banks into changemakers

Banks do not just respond to the economy; they help determine which businesses grow and which do not. Lending and investment decisions are based on expectations on which futures will exist. An institution that applies only risk-return criteria passively reinforces whatever systems currently generate the best short-term returns. In a world where harmful systems remain profitable, that mostly means financing harm. Banks need to build on their existing capabilities to assess the transformative potential of financing activities to create a greater impact.

A bank that wants to make a real difference needs to ask harder questions and sometimes back less obvious clients. This can mean lending to the farmer who is converting to organic agriculture with a crop that has not been certified before, the community-led energy cooperative, or the small manufacturer working with new biobased building materials. It may also involve a broader role for banks, like facilitating collaboration and generating cross-sectoral economic and transition insights.

We understand, also from our practice, that it is not always easy to ensure impact is transformative. Of course, this is also a call upon policy makers and society: if we had government policies aimed at phasing out fossil fuels, taxing pollution and subsidising the scaling up of sustainable practices, a transformation would be easier. Still, banks have the tools and the relationships to start making different choices and contribute to transformations.

If you want to know more, read our vision paper on changemaking (pdf).

End notes

1. Berk, J. B., & Van Binsbergen, J. H. (2025). The impact of impact investing. Journal of Financial Economics, 164, 103972. The impact of impact investing - ScienceDirect.

2. IPBES (2024). O’Brien, K., Garibaldi, L., Agrawal, A., Bennett, E., Biggs, O., Calderón Contreras, R., Carr, E., Frantzeskaki, N., Gosnell, H., Gurung, J., Lambertucci, S., Leventon, J., Liao, C., Reyes García, V., Shannon, L., Villasante, S., Wickson, F., Zinngrebe, Y., and Perianin, L. (eds.). Summary for Policymakers of the Thematic Assessment Report on the Underlying Causes of Biodiversity Loss and the Determinants of Transformative Change and Options for Achieving the 2050. Vision for Biodiversity of the Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services. IPBES secretariat, Bonn, Germany.

3. Meadows, D. (1997). Places to intervene in a system. Whole earth, 91(1), 78-84. http://www.wholeearthmag.com/ArticleBin/109.html

4. Abson, D. J., Fischer, J., Leventon, J., Newig, J., Schomerus, T., Vilsmaier, U., ... & Lang, D. J. (2017). Leverage points for sustainability transformation. Ambio, 46(1), 30-39.Leverage points for sustainability transformation - PubMed

5. Senge, P. (1990). The Fifth Discipline. The Art and Practice of Learning. Organization. New York, NY: Doupleday Currence.

6. Sengers, F., Wieczorek, A. J., & Raven, R. (2019). Experimenting for sustainability transitions: A systematic literature review. Technological forecasting and social change, 145, 153-164. Experimenting for sustainability transitions: A systematic literature review - Research portal Eindhoven University of Technology

7. Kishna, M., Niesten, E., Negro, S., & Hekkert, M. P. (2017). The role of alliances in creating legitimacy of sustainable technologies: A study on the field of bio-plastics. Journal of Cleaner Production, 155, 7-16. The role of alliances in creating technology legitimacy: a study on the field of bio-plastics - Vrije Universiteit Amsterdam

8. IPBES (2024).

9. Loorbach, D., Schoenmaker, D., & Schramade, W. (2020). Finance in transition: Principles for a positive finance future. Rotterdam: Rotterdam School of Management, Erasmus University. 2020_Finance_in_Transition.pdf