- Europe’s current linear economy (extract–use–discard) creates economic risk and dependency, with volatile raw material prices and supply chain instability threaten businesses and strategic autonomy.

- Large amounts of valuable resources, like e-waste, are lost, exported, or underused, even though recycling them domestically could be cheaper and reduce reliance on imports.

- As highlighted by the recent NVB position paper, the EU must start by fixing market incentives to make circularity competitive and support long-term resilience.

For years, we have argued that the traditional linear model (extract, produce, discard) is incompatible with a future that stays within planetary boundaries and ensures just resource extraction and equitable access.⁵ Now, it’s becoming more and more apparent that a linear future is also no longer compatible with economic resilience or strategic autonomy.

A structural economic risk

European businesses operate in an increasingly volatile resource environment. Prices of virgin raw materials, from copper and aluminium to lithium and rare earth elements, have experienced sharp spikes over the past years due to high demand, supply chain disruptions, geopolitical disputes and energy shocks.⁶ The demand for these materials is expected to more than double over the next two decades, since they are essential to renewable energy, digitalisation and electrification.⁷ Without addressing the scale of material demand, efforts to manage supply-side risks will remain inherently fragile.

From a financial perspective, this dependency and surging demand translate directly into risk: price volatility, supply disruptions, weaker margins and stranded asset exposure. Beyond firm-level risk, resource dependency also creates macroeconomic vulnerability through value chain disruptions that can reduce trade and inflate prices over the long term.⁸

Europe is throwing value away

The inefficiency of the EU’s current linear system is shocking, especially when looking at a concrete example like electronic waste. Europe generates around 10.7 million tonnes of e-waste each year (roughly 20kg per person).⁹ This waste stream alone contains an estimated 1 million tonnes of critical raw materials embedded in phones, computers, appliances and cables. Yet around 700,000 tonnes of this e-waste are landfilled or incinerated annually, while at least 400,000 tonnes are exported for reuse in other countries.¹⁰ In essence, Europe is exporting strategic resources it will later need to re-import, at higher cost and under greater geopolitical uncertainty.

The argument against collecting and re-processing these materials within Europe’s own borders is often cost. Collection, recycling and recovery systems remain incomplete and insufficiently scaled, but this is due to shortcomings in system design and long-term planning, not a fundamental lack of economic viability. Once expanded and modernised, these systems can significantly reduce material sourcing costs.

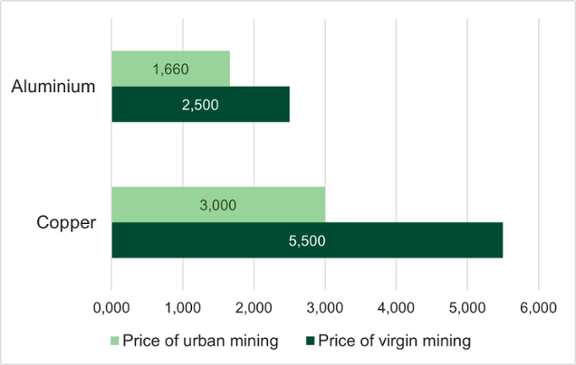

Copper and aluminium are an early example, where studies have found that extracting these materials from discarded products, infrastructure and waste is significantly cheaper than virgin mining.¹¹ The average cost of recovering copper and aluminium from urban sources is around $3,000 and $1,660 per ton, respectively (well below the $5,500 and $2,500 per ton required for virgin mining).

This price gap illustrates the tangible economic benefit Europe could capture through expanded domestic circularity. However, this cost advantage does not yet apply uniformly across all materials, as high-volume and relatively concentrated urban stocks (such as copper) are easier and cheaper to recover than more dispersed or lower-volume resources.¹² At the same time, even where secondary recovery is technically and economically feasible, its competitiveness is undermined by unfair pricing of negative externalities.

Figure 2: Cost comparison of virgin and urban mining for copper and aluminium

The illusion of cheap virgin materials

There seems to be a striking disparity, where on the one hand we overestimate the cost of re-processing secondary materials, but we also underestimate the negative externalities of virgin materials which are currently not reflected in their price. Circular approaches that carry low negative externalities usually involve higher initial costs to make products repairable, use recycled inputs, adopt modular designs, and support recovery and reuse.¹³

In contrast, the market price of virgin extraction rarely reflects the environmental degradation associated with mining and processing, such as habitat destruction, water depletion, soil contamination, biodiversity loss and significant greenhouse gas emissions.¹⁴ Nor does it capture the social costs of unsafe labour conditions, community displacement, and human rights risks in fragile regions.¹⁵ The market will not naturally adjust to reflect these true costs and doing so is essential to make circularity commercially viable.

Isolated measures are not enough

Europe already has circular frontrunners and scattered policy instruments, but isolated measures cannot create a functioning critical raw materials market. This is why a compelling, actionable vision for a competitive European industry of the future must begin with clarity about which materials and business models have a place in that future, and which do not. The upcoming EU Circular Economy Act is the ideal instrument with which to outline that vision.

The recent NVB position paper on the circular economy and the supporting explanatory paper fully back this view,¹⁶ calling for the European Union to correct market failures by:

- Implementing phase-out road maps for high-impact materials, such as PFHxA and ultra-low durability textiles. For other high-impact materials the focus should be on prioritising and restricting their use to essential applications.

- Setting minimum recycled content requirements for products containing critical raw materials with a high security risk, such as lithium, cobalt, rare earths, tin, and copper. These requirements complement existing or forthcoming mandatory recycled content targets (such as those for plastic packaging or textiles). This policy approach would boost recycling and the demand for its feedstock, cut demand for virgin extraction, and improve resource security.

- Expanding Extended Producer Responsibility schemes to include a full product lifecycle approach (such as that introduced in the 2023 for batteries) across a broader range of sectors.¹⁷ Such EPR is especially important in sectors with particularly large material footprints and long-term waste challenges, such as construction materials and wind turbine blades. These sectors are currently not covered, yet they are critical for Europe’s climate transition and generate substantial volumes of complex waste if not designed for reuse.

- Phase-out roadmaps for high-impact materials (like, PFAS and ultra-low durability textiles).These measures would not only harmonise market incentives, but would also fix the current regulatory patchwork faced by companies operating within the EU single market (where businesses face varied EPR, content requirements and product standards).

- Embedding resource conservation and circularity into EU financial architecture. A key part of this is explicitly and systematically integrating circular principles (durability, repairability, and recyclability) into the eligibility criteria for EU public procurement and financing instruments, such as the proposed Industrial Decarbonisation Bank.

While Europe recognises the strategic importance of securing raw materials and strengthening circularity, its internal market conditions are misaligned with those ambitions. Without regulatory correction, price signals will continue to favour short-term extraction over long-term resilience.

End notes

1. Onstad, E. (2026, February 27). Exclusive: GKN cancels plans for magnet factory in setback for Europe’s rare earth aims. Reuters.

2.Payne, J. (2026, February 2). EU efforts to diversify critical raw material imports fail so far auditors say. Reuters.

3. Muggah, R. and von Weizsäcker, R. (2025). The mineral wars–How Ukraine’s critical minerals will fuel future geopolitical rivalries. Center for International Relations and Sustainable Development; Peck, D. (2025) Critical Raw Materials. TU Delft Website.

4. European Parliament (2025, November 4). Suspension of silicon metal production in Europe and safeguards for industries linked to critical raw materials. European Parliament Website; Rory Elliott Armstrong, R. (2026, February 7). Stellantis-backed ACC shelves plans to open battery gigafactories in Italy and Germany. Euronews; 10+ (2025, September 29). Dutch plastic recycling industry struggles with cheap new plastic. 10+ Website.

5. Triodos Bank (2024, April 29). Transformative resource lifecycles: An urgent shift from linear to circular. Triodos Bank.

6. Khadan, J. and Temaj, K. (2025, December 16). Metal prices poised to strengthen further. World Bank Blogs.

7. Kowalski, P. and Legendre, C. (2023, April). Raw materials critical for the green transition. OECD Publishing.

8.Kohlscheen, E., Rungcharoenkitkul, P., Xia, D., & Zampolli, F. (2025). Macroeconomic impact of tariffs and policy uncertainty (No. 110). Bank for International Settlements.

9. G. Iattoni, S. et. al. (2025). 2050 Critical Raw Materials Outlook for Waste Electrical and Electronic Equipment. United Nations Institute for Training and Research.

10. G. Iattoni, S. et. al. (2025). 2050 Critical Raw Materials Outlook for Waste Electrical and Electronic Equipment. United Nations Institute for Training and Research.

11. Zeng, X., Xiao, T., Xu, G., Albalghiti, E., Shan, G., & Li, J. (2022). Comparing the costs and benefits of virgin and urban mining. Journal of Management Science and Engineering, 7(1), 98-106.

12. Gobbo, E. (2021). Understanding Urban Stocks. FutREuse.

13. United Nations Environment Programme Finance Initiative, & Circular Economy Leadership Canada. (2021). World Circular Economy Forum 2021 (WCEF2021) accelerator session focused on “Financing the circular economy transition.”

14.Stanimirova, R. (2024, October 2023). Mining Is Increasingly Pushing into Critical Rainforests and Protected Areas. World Resource Institute;Dehkordi, M. M., Nodeh, Z. P., Dehkordi, K. S., Khorjestan, R. R., & Ghaffarzadeh, M. (2024). Soil, air, and water pollution from mining and industrial activities: Sources of pollution, environmental impacts, and prevention and control methods. Results in Engineering, 23, 102729; Sinai. (2022, October 25). How to Address Scope 3 Emissions in the Mining Value Chain. Sinai Website.

15.UNEP-FI (2026), ‘Sector Profile: Minerals and metals extraction’. UNEP-FI.

16. Dutch Banking Association (2025, October). ‘Position paper: EU Circular Economy Act’. NVB.

17. EU Directorate-General for Environment (2023, August 17). Circular economy: New law on more sustainable, circular and safe batteries enters into force. European Commission Website.

18. Bauer, M. (2023). What is Wrong with Europe’s Shattered Single Market? Lessons from Policy Fragmentation and Misdirected Approaches to EU Competition Policy. ECIPE.