Characteristics of steward-ownership

Companies can structure their ownership and governance in different ways. Steward-owned companies are organised according to two principles²:

- Economic rights and voting rights are separated

- Profit allocation is purpose-driven

The first principle means that holding a financial stake in a company does not grant any control over its strategy or operations. In the traditional shareholder model, shareholders own (part of) the company and gain profit and decision-making rights. In steward-owned companies, these key decisions are instead made by designated ‘stewards’.³ Who those stewards are can vary. Unlike traditional shares, steward control cannot be sold or inherited.

The second principle dictates that profit is a means, not an end. Rather than always being distributed to the owners, steward-owned companies might reinvest their profits to advance the company’s purpose, or in some cases donate (part of) their profits to a charity. Profits may also be used to repay investors or be distributed as dividends.

How steward-owned companies work in practice

Just as conventional companies vary, so do steward-owned ones. Working for a small startup differs from a publicly listed company, and both can be steward-owned. For practical purposes, steward-owned companies often operate like conventional companies: they have budgets, managers, and clearly defined leadership roles. The key difference between steward-owned companies and conventional companies is the separation of voting and dividend rights.

Employees’ day-to-day may look very similar to that in any other company, but employees may experience a difference in the company’s long-term strategic orientation towards a mission. What that precise mission is might greatly affect what it is like to work for a certain steward owned company.

What are the potential benefits of steward-ownership?

Companies operate within a web of stakeholders with varied interests. They might obtain value from the company in multiple ways, and at times the interests of different stakeholders might align (win-wins). At other times, trade-offs arise, for example when allocating profits. Increasing employee salaries, donating to charities, lowering prices or raising compensation to suppliers and paying dividends to investors are at odds with each other.

Many existing companies are shareholder-owned.⁴³ This model developed in a time when capital was scarce and business risks were high.⁵ By promising returns for investors, shareholder-owned corporations managed to mobilise large amounts of capital for enterprise. Prioritising shareholder-interest presents an easy solution to stakeholder trade-offs: the shareholders’ interest dominates, always.⁶ What exactly these shareholders preferences are remains debated. Some economists such as Milton Friedman argue that firms should exclusively aim to maximise the financial return for shareholders.⁷ Others argue that shareholders could focus on broader objectives than just their own financial gain.⁸ Either way, shareholder primacy makes shareholders’ interest the core objective.

If shareholder value is maximised, profit and share price become a business’ targets. This can seriously erode long-term social and ecological value.⁹ As Katharina Pistor argues, the legal architecture of corporations including limited liability for investors reinforces this short-term financial focus.¹⁰

Steward-ownership is one way to move corporations from narrow shareholder focus towards a mission-orientation by shifting decision-making power.¹¹ Trade-offs still exist between various stakeholders interests (e.g. lowering prices for consumers, raising wages for employees, or generating profit for donation), although a clear mission can help prioritise between them.

Increasing interest for steward ownership

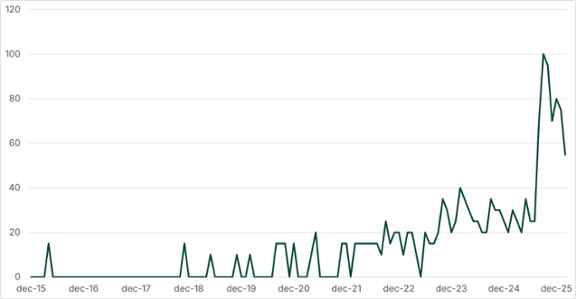

Search results for ‘steward ownership’ increased since early 2022, peaking in late 2025.¹² This signals increasing curiosity for the concept.

Figure 1: Google searches for ‘steward ownership’ (source: Google Trends worldwide)

Whether online attention translates to adoption is harder to determine. Since steward ownership is not a separate legal category in most countries, there is no central registry in which to check its prevalence. Anecdotal evidence seems to suggest that the concept is indeed gaining momentum: in the Netherlands and Belgium, support organisations We Are Stewards and Steward Owned both report an increase in the number of companies exploring steward ownership.¹³ ¹⁴ However, it still remains a niche phenomenon within the corporate landscape.

Organising steward-ownership: legal forms and governance structures

Those who are attracted to the concept of steward ownership face a practical challenge: in EU-countries, no dedicated legal form exists for it. Therefore, steward-owned companies rely on existing national legal forms, which are adapted or combined to create specific ownership restrictions and governance structures that approach the principles of steward-ownership. For example, a foundation can be established to hold the shares that carry the voting rights of a company, thereby exercising control over the company as the ‘steward’. Another option is the golden share model, where certain shares hold veto powers over specific significant decisions, such as selling the company.¹⁵ Due to their veto power, these shares can help safeguard a company’s mission and ownership, even if they represent only a small portion of all shares.

Both the European Parliament and the Dutch government (pdf) wish to develop a separate legal form for steward ownership (though at the EU-level the plans were not taken up by the European Commission). Apart from underscoring the increasing attention for steward ownership, these plans for the introduction of a ‘ready made’ legal entity may make it easier to start a steward-owned company.

Stock-listed steward-owned companies

Steward-owned companies can also be stock-listed. Their shares on public markets hold little or no voting rights. Stewards can be the entrepreneurs or employees of a company, but can also be external people somehow connected to the mission. In general, stewards will obtain voting but no or little dividend rights.

Financing steward-ownership

Early-stage financing of steward-owned organisations is most challenging. This is when income is low and the needed investment needed is risky, often financed through various rounds of equity sales. In these transactions, investors obtain partial ownership over the company including voting and dividend rights in exchange for financial capital. This traditional route is not available to steward-owned companies, because they do not want to (permanently) link dividend and voting rights.

Steward-owned companies solve this with novel financing instruments, such as profit-participating loans. These types of loans are (partly) paid back by receiving a pre-determined share of the profits of an organisation. They might run for a specific time, or until a certain factor of the principal is paid back. Another option is emitting shares without voting rights and with limited total dividend rights. Sumthing has raised money from investors in this way across three investment rounds. Half of the profit generated by the company is used to pay out dividends, until the dividend cap for a ‘shareholder’ is reached. Using cumulative preferred shares, which give investors a fixed annual entitlement to dividend without voting rights, is also an option. Sprinklr used this option, including the possibility to ‘pay off’ the shares. Multiple impact-oriented venture capital funds have already invested in steward-owned organisations, as have government funds.¹⁶ The Purpose Foundation reports over 250 million euros in investment capital has already been directed towards steward-owned companies. While these alternative forms of financing are still relatively niche, they show that steward-ownership and risk-bearing external financing are not mutually exclusive.

When established, steward-owned companies can obtain loans just like ‘normal’ companies, as loans typically do not affect ownership or governance. Access to credit mainly depends on the usual factors, such as the financial viability of a business plan and availability of collateral.

Initial conclusions – steward ownership in practice

We have discussed the principles underlying steward-ownership and the theory behind it. But does it work in practice? We draw some initial conclusions about what steward-ownership can and cannot do from real-life examples.

Conclusion 1: Steward-ownership can succeed in keeping a company oriented towards its mission in the long-term

Steward-owned companies succeed at prioritising their mission, across multiple ways of organising. Patagonia grants all voting rights to a perpetual trust and all profits to a charitable collective. Ecosia granted a ‘Golden Share’ to the Purpose Foundation. This Golden Share comes with veto rights which means that the Purpose Foundation can block profits going to anything else than combatting deforestation as well as attempts to sell control of the company to people not directly involved in its operation.

Conclusion 2: Steward ownership can be used for any mission

While steward-ownership provides a way of ensuring long-term commitment to a company’s mission, opinions might differ about whether that mission is worthwhile. We imagine that not many people will object to Sumthing’s mission to restore nature. Yet, some people might feel that Carlsberg’s mission of brewing ‘beer for a better today & tomorrow’ carries little societal value. Luxury watchmaker Rolex, also steward-owned, is sometimes used to ridicule the desirability of steward-ownership. Will luxury watches solve the world’s problems?

This might make you feel like steward-ownership is useless. If it can be applied for any mission, how does the model then help to prevent corporate misbehaviour?

We think this is the wrong conclusion. The innovation of steward-ownership is not that it divides the world into ‘good’ and ‘bad’ missions. Rather, it breaks the link between financial profit and corporate control, to ensure that the pursuit of profit does not become more important than the mission of a company.

Conclusion 3: Competitive markets exert pressure, even on steward-owned companies

Novo Nordisk’s mission is to “drive change to defeat serious chronic diseases”, aiming for long-term health rather than quick-fixes. Yet it produces Ozempic, a weight-loss drug sometimes criticized as a quick fix for the current obesity pandemic. When the company appeared to be losing ground in the competitive market for weight loss medication in 2025, the stewards of the Novo foundation fired part of the executive board. The new CEO stated that he wants Novo to ‘think more like Amazon’ and pursue more aggressive marketing strategies to maximize the sales of Ozempic.

Ethical clothing brand Patagonia faced similar tensions: despite its core values including justice, it has received public criticism for producing clothes in the same factories and under the same deplorable conditions as fast-fashion brands like Nike and Primark. Patagonia responded by setting improvement targets, but also signalled its inability to single-handedly eradicate these industry issues as a single player.

These examples illustrate that steward-ownership can strengthen a company’s long-term orientation and commitment to its mission, but is not a silver bullet. Competitive pressures sometimes still lead to compromises. While steward-ownership helps, we still need other fundamental reforms in our economic system to really facilitate a just and sustainable world.

Conclusion

The core premise of steward ownership is simple: by separating economic and voting rights and by using profit for purpose, a company’s mission becomes its focus. Here we immediately see both the strength and the limitations of steward ownership. By design, it encourages longer-term, mission-oriented thinking, something that is sorely needed to realise a just and sustainable economy within planetary boundaries. However, steward ownership itself does not prescribe which type of mission is worth pursuing. The concept provides us with a type of governance, not a set of values.

In practice, companies that aspire to this ownership model face several challenges. Founding a steward-owned company requires creativity in legal form and in raising early-stage financing, because traditional models do not fit its principles. Just like ‘normal’ companies, steward owned companies are sometimes faced with competitive market pressures which can push them to compromise on their mission. All in all this makes steward-ownership a useful tool in building a new economy, not a silver bullet.

End notes

[1] It is hard to quantify exactly how dominant, but hegemonic seems a fair description. For example, the OECD Corporate Governance Factbook 2025 exclusively considers variations of shareholder-owned companies. See: OECD (2025), OECD Corporate Governance Factbook 2025, OECD Publishing, Paris, https://doi.org/10.1787/f4f43735-en.

[2] Sanders, A., & Neitzel, N. (2025). Steward Ownership-Concept, Potential and Implementation in Germany and the Netherlands. Available at SSRN 5178366.

[3] Companies can also be employee owned, which is different from steward owned. Employee-ownership is outside of the scope of this article.

[4] The exact legal form differs per country and, in some cases, local law mandates an involvement of other stakeholders in the governance. Works councils, for example, are mandatory for companies of a certain size in some countries. In general, however, most corporate forms across countries are a variation of shareholder ownership, with shareholder interests gaining primacy over other stakeholders’ interests.

[5] Petram, L. O. (2011). The world's first stock exchange: How the Amsterdam market for Dutch East India Company shares became a modern securities market, 1602-1700

[6] Multiple companies with shareholders are not purely shareholder-focused. They find ways to anchor their mission or specific stakeholder interests in their governance. These could be Works Councils to represent employees, for example, but also foundations with special voting rights to protect a company’s mission.

[7] Friedman, M. (1970). The Social Responsibility of Business is to Increase its Profits. New York Times Magazine, September, 13, 122-126.

[8] Hart, O. D., & Zingales, L. (2022). The new corporate governance (No. w29975). National Bureau of Economic Research. Working Paper.

[9] Sjåfjell, B., & Taylor, M. B. (2019). Clash of norms: Shareholder primacy vs. sustainable corporate purpose. International and Comparative Corporate Law Journal, 13(3), 40-66.

[10] Pistor, K. (2019).The code of capital: How the law creates wealth and inequality.

[11] Sanders, A., & Neitzel, N. (2025). Steward Ownership-Concept, Potential and Implementation in Germany and the Netherlands. Available at SSRN 5178366.

[12] Some specific developments might have peaked interest to search for the concept, such as Patagonia’s announcement to become steward-owned. Search results for steward ownership originate mostly from the Netherlands, though variations on the term (e.g. foundation owned) and translations (e.g. propriété responsible, propriedad responsable, verantwortungseigentum) show increasing searches originating from the US, Germany, France, Spain and several South-American countries as well.

[13] https://www.awvn.nl/arbeidsverhoudingen/publicaties/steward-ownership-spdi/

[14] Information obtained in a private interview with Peter Depauwe from Steward Owned(February 5th, 2026)

[15] Armeni, A., Lyon, C., & Menter, J. (2023). Alternative Ownership Enterprises: An Introduction for Mission-Oriented Investors.

[16] Van Lathem, J. & Depauw, P. (2024). Steward-ownership. Duurzame economische groei via alternatieve ondernemingsvormen.